The Employees’ Provident Fund remains the most popular retirement saving tool for the majority of Indians. Of late, there has been an increase in the number of claim rejections, putting investors in a quandary. We tell you what can lead to such rejections and what you can do to deal with or avoid such a situation

Early in February, the Provident Fund (PF) office at Kaloor in Kochi, Kerala, went into a tizzy, when an old man was found to have consumed poison on the premises. That was the day when K.P. Sivaraman, a 69-year-old who had become almost a permanent fixture at the office for the last nine years in the hope of getting his Employees’ Provident Fund (EPF) balance disbursed, lost all hope, and decided to end his life. He was rushed to a hospital, where he breathed his last after a few hours.

His PF application was continuously rejected over the last nine years for some technical reason or the other and he was last told to produce his school certificate, which he couldn’t procure as his school did not have old records. Ironically, the PF was paid out a month later to his wife without the need for any additional document, except the ones that nominees are expected to submit.

Any organisation that employs 20 people or more has to mandatorily register with the Employees’ Provident Fund Organisation (EPFO). According to official data from EPFO from financial year 2022-23, out of 7.38 million claims received for final PF settlement, 33.8 per cent (2.49 million) were rejected, while 4.66 million were settled.

The rejection rate in 2022-23 is significantly higher compared to previous years, with rejection rates of around 13 per cent and 18.2 per cent in 2017-18 and 2018-19, respectively. The rejection rate continued to rise in subsequent years, reaching 24.1 per cent in 2019-20 and 30.8 per cent in 2020-21 for final settlement claims. In the financial year 2021-22, the rejection rate further increased to 35.2 per cent for final settlement claims.

An email sent by Outlook Money to Neelam Shanti Rao, Central Provident Fund Commissioner, EPFO, Ministry of Labour and Employment, Government of India, where we asked her about the reasons behind the increasing rejection rates of EPFO claims, what one can do to ensure EPF claims are not rejected, and the way out, did not elicit any response till the publishing of this story.

The Kerala suicide case shook the nation and led to a storm on the social media, which was flooded with complaints of rejected EPF claims. We spoke to many EPF subscribers, who have faced similar issues, to get to the heart of the problem and to find the way out.

Why Is EPF Popular?

For many individuals in India, EPF is still the sole source of retirement income. One of the reasons for that is the fact that people retiring now started working at a time when there were fewer other instruments that could help them accumulate a retirement corpus. For most, rejection of PF means being deprived of their life’s savings at a time when they need it the most.

Says Abhishek Kumar, a Securities and Exchange Board of India-registered investment advisor (Sebi RIA), and founder and chief investment advisor of SahajMoney, a financial planning firm: “EPF is a mandatory saving option for people earning Rs 15,000 or above per month. It comes with an implicit sovereign guarantee which makes it a practically risk-free investment option and has tax benefits. No wonder people rely on it for their rainy days or for retirement.”

At present, the return on EPF is 8.15 per cent. With a monthly contribution of 12 per cent each by the employee and employer, the scheme which is valid for the entire work-life of an individual, provides a decent corpus on retirement.

“Although, unlike fixed term deposits, EPFO does not declare the interest rate of EPF corpus in advance for the entire term, it is declared by the government every financial year. Also, the interest on the corpus is computed monthly and earns compounded interest, or interest on interest, every year so that after a while the interest earned on EPF corpus becomes much more than the annual contribution one makes,” says Kumar.

Since it provides a reasonable rate of return and is backed by the government, many also opt for Voluntary Provident Fund (VPF), which allows employees to make additional contributions to their EPF accounts.

Adds Kumar: “EPF is a great investment option for one’s long-term debt portfolio as it is risk-free and provides tax-free return which is difficult to generate through any other long-term debt option on a post-tax basis without taking additional risk. These benefits make it an obvious recommendation.”

It’s tax status indeed makes it attractive. EPF contributions are eligible for deduction of up to Rs 1.5 lakh under Section 80C of the Income-tax Act, 1961. From April 1, 2022, any interest on employee contribution up to Rs 2.5 lakh is tax-free, but interest earned on contributions above the Rs 2.5 lakh limit is taxable in the hands of the employees. Also, there is no tax to be paid on the withdrawal amount when the balance is withdrawn after five years of continuous service.

The fact that it offers partial withdrawal facility and allows withdrawal at the time of job change is also a plus. One can make partial withdrawals from their EPF account under special circumstances, such as medical emergency, wedding, education, purchase, and construction or repair of house. One can also make a partial withdrawal two months after one leaves a job and is still unemployed.

During Covid, when many people faced job losses, a new rule was introduced where employees could withdraw three months of their basic salary plus dearness allowance or 75 per cent of the total accumulated amount, whichever is lower. A full withdrawal is allowed if someone remains unemployed for over two months.

Now, with problems of delayed or rejected withdrawal cases cropping up, it’s popularity has come into question.

Why Are EPF Claims Rejected?

The Technical Story: Though EPF offered an olive branch to subscribers during the Covid period, the rejection rate even then was quite high, as mentioned earlier in the story. But what could be the reasons behind rejections? We did a little digging to find out.

One of the major reasons is the complete shift to the online system for processing claims, says Shweta Rajani, head, mutual funds, Anand Rathi Wealth. She explains: “Previously, document verification for claims primarily occurred at the employers’ end before reaching EPFO. However, with the shift to Aadhaar-linked online processing, 99 per cent of the claims now go through the online portal.”

As a result, any small discrepancy could lead to rejection. In fact, EPF authorities commonly reject claims due to administrative or documentation errors.

Pratyush Miglani, managing partner, MVAC Advocates & Consultants, a New Delhi-based law firm, says one of the main reasons why one’s EPF claim may be rejected is incomplete or erroneous documentation. “Instances of missing signatures, incomplete forms, or discrepancies in the provided information can hinder the processing of claims, which highlights the critical importance of meticulous attention to paperwork,” he says.

Failure to furnish requisite identification documents or updated personal information, and inadequate completion of know your customer (KYC) requirements may also be a barrier to EPF withdrawal claim approvals.

Another challenge arises from discrepancies between the details furnished by the employer and those registered with the EPFO. Inconsistencies in particulars, such as the spelling of the name, date of birth, or Aadhaar card may trigger rejection.

“Instances of employer non-compliance, wherein requisite contributions are not duly remitted, or accurate employee details are not reported, pose issues in the smooth processing of EPF claims. Such lapses underscore the importance for employers to adhere closely to statutory obligations,” says Miglani.

Also, premature withdrawals are subject to certain terms and conditions. Failure to comply with such rules may lead to claim rejection. Finally, providing incorrect or outdated bank account information can result in the rejection of EPF withdrawal claims.

The People Story: Individuals who have faced claim rejections have a different story to tell. Many of them shared with Outlook Money that quite like Sivaraman from Kerala, their claims were rejected even after they rectified the errors. Soumyasanta Roy, 40, who works with a private company in Kolkata, says that four of his claims were rejected consecutively, from the same EPFO Office at Bandra (he started his career in Mumbai). Two of them were for partial withdrawals for the renovation of his house in June 2022. He made two attempts for partial withdrawal, but both were denied for different reasons. Two other requests were meant for EPF transfers when he was changing jobs, and these were denied, too.

Soumyasanta Roy

Age 40

Kolkata, West Bengal

Four of his claims were rejected by the EPFO office in Bandra (Mumbai). Two were for partial withdrawal for the renovation of his house and two were for transfers when he was changing jobs. All four claims were rejected.

***

Different reasons were given each time, some of which he saw as frivolous. In one case, the father’s name was different (this claim is already settled), in the second the member’s name was not printed on the cancelled cheque. For this one, he wrote a letter to the Bandra (Mumbai) PF commissioner on September 21, 2023, and got a reply: “Your grievance has been referred to the concerned section for further necessary action. Same will be taken in due course of time.” The claim hasn’t been settled till date.

Soumyasanta says that the problem is that the EPFO website is designed poorly and is not user-friendly. “It does not allow the subscriber to respond to the rejections or provide clarifications. Once a claim is rejected, one needs to start afresh. Even if you fix the problems highlighted in the rejection, the office will provide new reasons in your next submission,” he says.

Some key details, such as the father’s name cannot be updated online, and subscribers need to send the forms to the EPF office. If the head office is in another city, then you will have to send it by post and there is no guarantee of receiving an acknowledgement or confirmation or any other means of tracking your request. “Overall the process is archaic,” says Soumyasanta.

Many have also faced rejections when withdrawing their PF after changing jobs and things have not been sorted even after they did what they were asked to do.

Says Rahul Chhabra, a 50-year-old freelance writer, based in Delhi, “I had to withdraw my PF after changing my job. The human resources (HR) team instructed me to apply online using my Universal Account Number (UAN). Initially, I was unaware that I needed to submit Form 15G along with my application. Instead, I was advised to send the copy of a blank cheque and a soft copy of my Permanent Account Number (PAN). Unfortunately, my first application was rejected, citing the absence of Form 15G.”

In the next attempt, he included Form 15G, his PAN, and another blank cheque, but the application was flagged for review. After multiple unsuccessful attempts online, he sought assistance from his former HR team. They discovered that an objection was raised by the EPF department regarding family pension deductions, which he was ineligible for as his basic salary exceeded Rs 15,000. The HR team clarified this with the EPF and requested a correction.

“Although a month has passed since the ticket was generated and the complaint was submitted, the funds are yet to be transferred to my bank account,” says Chhabra.

There are multiple complaints of claim rejections by EPF subscribers, according to their testimonies on social media. Some of the cases have been pending for months, others for years. For instance, Deep Sondhi, who has been jobless for the last two years, posted on micro-blogging site X that his claim has been under process even after two years, and all the relevant phone numbers he has tried to reach are constantly busy.

Mumbai-based Rahul Rao, who did not want to reveal his real name, says he applied for partial PF withdrawal multiple times, but they were rejected without any valid reasons. In the most recent instance, when the 45-year-old visited the Vashi office after about two months, he was asked to raise the claim again, which he did; however, he has been waiting for the claim for six months since starting the process.

What Should You Do?

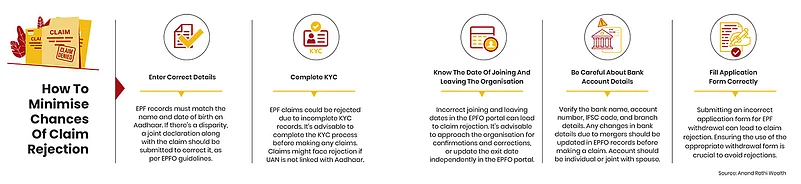

Before Filing For Withdrawal: To ensure a smooth EPF claim process and avoid rejection, EPF members must pay attention to details and update them carefully in their EPFO records. Here are some key details to take note of.

- Past Employment Details: “Provide accurate information about all past employment details, including joining and exit dates, employer details, and any gaps in service. It’s essential to ensure that this information matches the records maintained by the EPFO,” says Abhishek Soni, CEO, Tax2Win, an income tax portal.

- Universal Account Number (UAN): Activate and regularly update your UAN with current employment details. For EPF members across different employers, UAN serves as a unique identifier. The claim process would be smooth and there could be seamless tracking of EPF contributions provided you keep it updated. It may be noted that the EPFO recently introduced a system for automatic transfer of an employee’s PF balance in the UAN when they switch employers.

- Bank Account Details: For EPF withdrawal, you must verify and double-check the bank account details. To avoid any issues with fund transfers, you must ensure that the account number and IFSC code are correct. A common reason for claim rejection is entering incorrect bank details.

- ID And Address Proofs: The information in the EPFO records must match the details in your ID and address proofs, which should include your name, date of birth, father’s name, gender, and other relevant details. You must regularly review and update these details as necessary.

- Member Sewa Portal: To access and review your EPFO records, you must utilise the Member Sewa portal. Says Soni: “While this portal gives you important insights into your profile information, it also allows you to make necessary updates or corrections. You must stay informed about your EPF account status and regularly log into your portal.”

- Nomination Update: Your nomination details must be updated properly. In case of the member’s demise, it is important to specify beneficiaries who would receive the EPF corpus. You must regularly review your nomination details as per your current preferences.

- Inform Banker And Employer: “For verification of the claim and other details in some cases, the EPFO authenticates with the banker and the employer. The individuals can always inform their banker and employer upfront to provide their confirmation swiftly and fast-track the process,” says Akhil Chandna, partner, Grant Thornton Bharat.

After Encountering A Rejection: Don’t give up if your claim is rejected. Instead be systematic about raising the issue.

- Identify The Reason: “The online portal should provide the reason for rejection. Then, address the specific issue mentioned,” says Rajani.

Inaccurate documentation, mismatched signatures, or bank details are common reasons for rejection. “For instance, the name on your EPF files may not match the name on your Aadhaar card,” says Anant Ladha, founder, Invest Aaj For Kal, a financial advisory firm.

- Document The Issue: Vipul Jai, partner, PSL Advocates and Solicitors, says that if individuals encounter technical difficulties owing to server issues while trying to withdraw EPF money, they should contact EPFO through their helpline or online portal to report the issue. It is always advisable to document the issue, including screenshots of the error message, to better address the problem.

- Fix The Error: The next step is to ensure all data is in place, fix any errors, and resubmit your claim. If the issue persists, contact your local EPFO office or helpline for guidance. “If the reason for rejection or technical glitch is unclear, it would be prudent to contact the EPFO to better understand the reason before taking any steps,” says Jai.

- Raise A Grievance: “In case the steps taken do not return the desired result, file a complaint through EPFO’s grievance redressal mechanism,” says Jai.

The EPFO has established an online portal—the EPFiGMS (https://epfigms.gov.in/)—to address the grievances of members. The EPFiGMS portal allows members to raise their grievances or issues and direct them to the relevant office to which their UAN is tagged.

“The portal also provides an option to send grievances to the head office in Delhi. Individuals should promptly file their grievances on the EPFiGMS portal and track the status of the complaint. The EPFO’s latest published Citizen Charter states that grievances on the EPFiGMS will be settled within seven working days, failing which the grievance will be escalated to a higher authority,” says Bishen Jeswant, partner, Cyril Amarchand Mangaldas, a law firm.

But Soumyasanta has had a different experience. He says that any grievances submitted through the redressal system ends up with the same office against whom the grievances are raised. And they simply close the grievance by providing a canned reply like “We are looking into it.” He saw this reply on the grievance portal.

- The Last Resort: If that is indeed the case, the last resort is to go for legal recourse. If necessary, individuals can seek legal assistance to understand their rights and options for challenging the rejection of their EPF claims. “Legal experts can provide guidance on the relevant laws and procedures and represent individuals in legal proceedings if required. Further, individuals also have the option to take legal action against the employer or EPFO for wrongful rejection of EPF claims. This may involve filing a civil lawsuit seeking damages or other appropriate remedies,” says Miglani.

The legal rights of individuals whose EPF claims have been repeatedly rejected without valid reasons are primarily governed by the Employee Provident Funds and Miscellaneous Provisions Act, 1952, but there are some other remedies which can also be availed of by the employee (see Types Of Legal Remedies).

The Way Forward

According to experts, there are several systematic improvements currently in the pipeline that would go a long way in streamlining the EPF claim process, including superior technology upgrades, proactive data cleaning to minimise foreseeable errors, and proper KYC.

Nita Menezes, founder and CEO of Financially Smart, a financial planning firm, says that to reduce claim rejection rates and enhance member experience, EPF authorities should focus on enhanced digital infrastructure for streamlined processing, improved validation mechanisms to minimise errors, and transparent communication channels for timely feedback.

Regular training programs for staff to ensure compliance and simplified procedures and documentation requirements will also make a difference, she adds.

Says Shashank Pal, chief business officer, Prabhudas Leeladhar Wealth Management, a financial advisory firm: “Mandating multiple proofs simultaneously, for identity confirmation, improves the chances of accuracy. Linking with Aadhaar should eliminate most of the glitches. EPF is usually the entire life’s savings for most subscribers, making it susceptible to high risk if a high degree of due diligence is not exercised by all parties. The EPFO must establish the identity of the subscriber firmly before it is credited to them.”

To sum up, the only way out as of now is to be careful about entering your details when submitting your claim withdrawal application and follow it up meticulously in case any discrepancies need to be corrected. However, if your claim is still rejected, be persistent in pursuing for a resolution.

meghna@outlookindia.com