If you are buying a health insurance cover, ideally, you should have one that provides a minimum coverage of at least Rs 20 lakh, if not more. However, this would also mean super expensive premiums. The only way you could get high coverage and pay low premiums is by way of a top-up or a super top-up health plan. And most people get confused between these two aspects.

Explains Rakesh Goyal, director, Probus Insurance Broker: “Considering the ever-increasing medical expenses, having an insurance policy with either a top-up or a super top-up plan is an added advantage, as both these plans help in increasing your sum insured amount above your base policy. Such plans ensure additional coverage in case of medical emergencies, and also come with tax benefits. Having said that, the motive behind both these plans would be to provide extra financial support, but they do have certain coverage differences as well.”

If you are planning to buy a top-up health plan or a super top-up health plan, you should ideally know the difference between the two.

Difference Between A Top-Up And A Super Top-Up Health Plan

Top-up and super top-up plans are both geared towards providing higher insurance coverage with low premiums. The main difference between a top-up and a super top-up policy is in the manner the deductible chosen under the policy is applied.

A top-up plan is a high-deductible health plan which pays for in-patient medical expenses in excess of the prescribed deductible limit.

The super top-up plan is similar to the top-up plan, except that in the top-up plan, the deductible is applied on each and every claim, whereas in the super top-up plan, the deductible will apply on an aggregate basis towards hospitalisation expenses incurred during the policy period.

The premiums and out-of-pocket expenses under both plans may also differ. The deductible, if applicable on each claim, in case of a top-up policy, may lead to high out-of-pocket expenses.

Hence, for both top-up and super top-up health plans, health insurance provides cover above the threshold limit or deductibles. When it comes to the number of claims, top-up health plans include single claims above the deductible limit, whereas super top-up health plans include cumulative bills during a policy term once it exceeds the deductibles.

For top-up health plans, deductibles are paid on every claim, and for super top-up health plans, the deductibles are paid once in a policy year.

Explains Shreeraj Deshpande, head, health businesses, SBI General Insurance: “Super top-up plans may or may not be high on premiums, but allows utilisation of the sum insured once the deductible limit (in aggregate for all the claims) for the policy year has surpassed. Therefore, for the same sum

insured and deductible chosen, the super top-up plan is more beneficial for the customer than a top-up plan.”

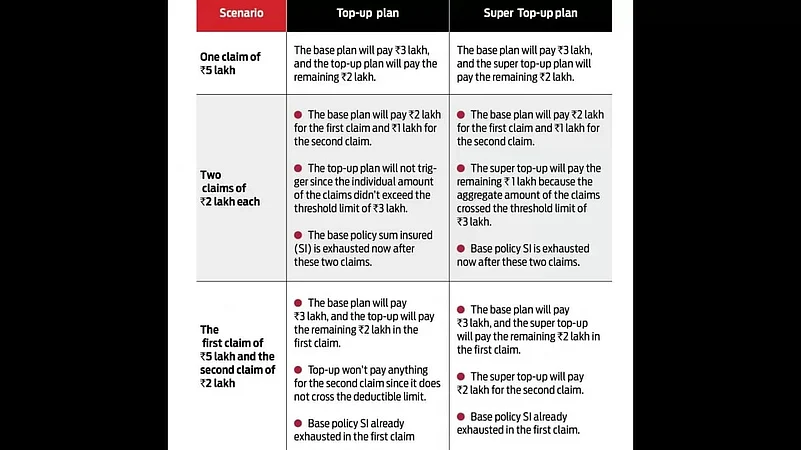

Assume that the sum insured for your base policy is Rs 3 lakh.

If you take a top-up or a super top-up of Rs 10 lakh with a deductible of Rs 3 lakh, let’s see how the claims will be paid in both options.

Deductible In Top-Up/Super Top-Up Plans

Deductibles refer to the limit set by health insurance companies. It acts as a safety net for the insurance company and prevents people from filing frequent and trivial medical claims.

This amount needs to be borne by the policyholder. Deductibles are not covered by health insurance providers. They only pay the amount over and above the deductibles. Basically, the amount of deductibles need to be paid by you, and the remaining amount i.e., the excess is paid by the insurer up to the limit of the sum insured.