The topic of goods and services (GST) tax on house rent drew significant attention after queries on whether salaried individuals should pay GST on home rent flooded social media.

“I have received this email about the applicability of GST on my property rent from next month”, wrote one of the social media users. Apparently, the landlord is a housing company that has contracted multiple flats from property owners for rental purposes.

But is the company right in charging GST on house rent? And does the law permits it?

Here’s what experts say.

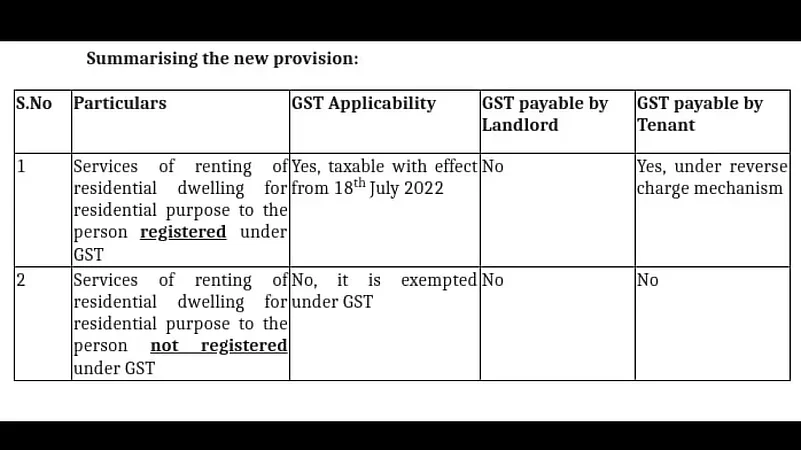

Archit Gupta, founder and CEO of Clear, a tax-filing assistance company, clarifies that until July 17, 2022, GST was not charged on renting or leasing residential properties. However, from July 18, 2022, on the recommendation of the 47th GST Council meeting, it was decided that “GST shall be charged if it (residential property) is rented or leased by a GST-registered person.”

Why Was This Person Asked To Pay GST?

The individual claimed that the rental company asked him to pay GST, although he is a salaried person. He was also not clear whether he or the landlord should pay GST.

Seeking to clarify these doubts, Bhavya Sharma, a company secretary, lawyer, and founder of business consultancy firm Bhavya Sharma and Associates (BSA), explains that “18 per cent GST will be levied on residential property rent under the Reverse Charge Mechanism (RCM).” However, a salaried individual not registered under GST need not pay any taxes as it applies only to tenants registered under GST, she adds.

More Clarifications Regarding GST on Rent

Another salaried individual, who is GST-registered and provides consultancy services part-time from his rented home, wanted to know if he should pay GST on his home rent.

Clear CEO Gupta tries to answer his predicaments with an example. Gupta said that suppose the person is a gig worker or consultancy service provider or e-commerce seller, working from his rented home, he’s using the place only for residential purposes - without appropriating the rental expense as a business expense deduction in an income tax return. In such a scenario, he can still refrain from paying GST on a reverse charge basis.

“However, if you show this rental expense as a deduction for income tax purposes, then be sure to compute and pay GST regularly in the monthly/quarterly GST returns you file. Note that where you are registered as a composition taxable person. Here, you cannot claim the input tax credit on rental expenses but might still have to pay GST on rent on a reverse charge basis,” adds Gupta.

When Can Input Tax Credit Be Claimed On GST On Rent?

Gupta explains that as per the update in the law, a GST-registered tenant “should pay GST on a reverse charge basis. It means tenants themselves must calculate GST at 18 per cent on the rent or lease amount and deposit it with the government on the GST portal. They can claim this value as a deduction while they pay tax on sales in GST returns.”

Sharma clarifies that in case the residential property tenant is registered under GST but the landlord is not, then the tenant will be liable to pay 18 per cent GST under RCM and he may claim an input tax credit on the same.

Sharma further notes that if the residential property owner is GST-registered but the tenant is not, and neither is a salaried person, this transaction will be exempt from GST.

Gupta explains that under the GST law, persons include both individuals and corporate entities. Hence, registration is needed when the person owns a business or has a profession that makes an annual turnover of more than the threshold limit as defined under the law.

The annual turnover limit varies according to the nature of the supply, and the state or the union territory (UT), where the principal place of supply is located.

For persons rendering only services, the limit is Rs 20 lakh in a financial year. For goods suppliers, the limit is Rs 40 lakh, and for persons in north-eastern or special category states, the limit is Rs 10 lakh.

When Does The Provision of Tax Deducted At Source (TDS) Apply On Rent?

While the landlord will collect GST from the tenant and deposit it, the tenant will have to deduct income tax at source (TDS) if the property rent exceeds Rs 2.4 lakh annually, applicable from the assessment year 2020-2021. However, no GST is to be charged on such rent.