Breast, cervical, and ovarian cancer are the most common types of cancer that affect women and see the highest number of insurance claims. Prevention and a health cover can help you fight the disease

Actor-model Poonam Pandey took social media by storm in February this year, when a statement from her social media handle announced her death due to cervical cancer. The statement, as it turned out, was fake and it was later claimed that it was meant to be part of a campaign to spread awareness about the threat of cervical cancer among women.

Pandey was criticised for her “deceptive stunt”, but it indeed brought the discussion around the threat of cancer to women to the limelight.

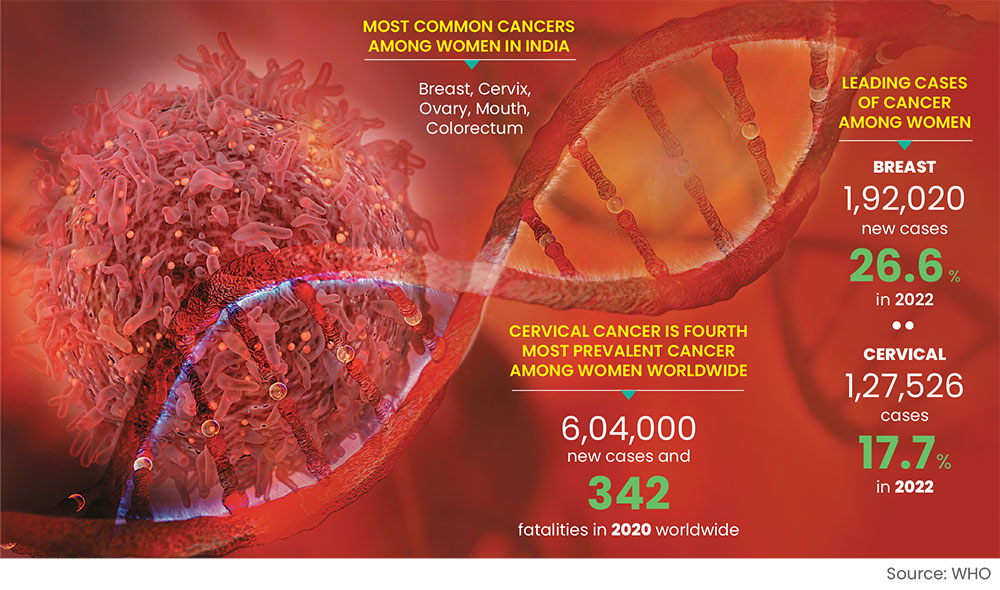

According to the World Health Organization (WHO), cervical cancer ranks as the fourth most prevalent cancer among women worldwide, with around 604,000 new cases and 342,000 fatalities recorded in 2020.

Data around another type of cancer that is common among women—breast cancer—is equally scary. Breast cancer was the leading cancer among women with as many as 192,020 new cases (26.6 per cent), followed by 127,526 cases of cervical cancer (17.7 per cent) recorded in 2022, according to data from the WHO.

According to the WHO, women in India were found more prone to breast, cervix, ovary, mouth, and colorectal cancer.

Treatment of cancer could involve various medical procedures, such as surgery, chemotherapy, radiation therapy, and medication. These treatments can incur significant expenses, including hospital bills, doctor’s fees, diagnostic tests, and prescription drugs, which can put enormous stress on one’s finances.

Left unprepared, it can potentially wipe away one's entire savings.

We give you a lowdown on preventive care as well as the insurance policies that can come to your rescue, in terms of finances, if any type of cancer were to strike you.

Prevention Is Better Than Cure

A healthy lifestyle is something that is always recommended, but there have been several cases where that did not have a bearing on the condition.

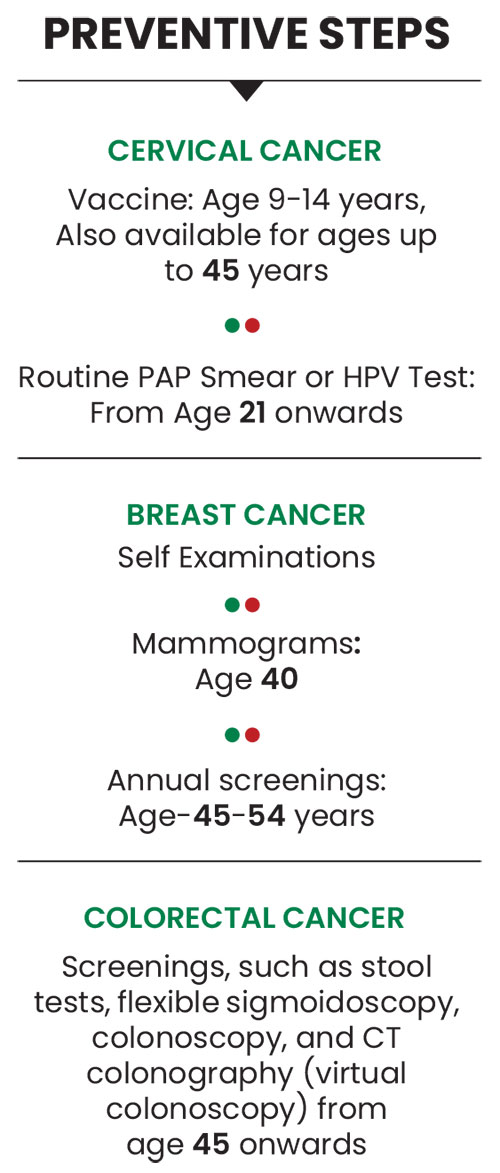

But there are some preventive steps you can take for certain cancers. Cervical cancer is a case in point, as it can be prevented with a vaccine. “The vaccine against cervical cancer is called Human Papillomavirus Vaccination (HPV). The preferred target age group for HPV is 9-14 years. However, there are vaccinations available for ages up to 45 years as well,” says Santosh Puri, senior vice president, health product and process, Tata AIG General Insurance.

The cost of the vaccine depends on the number of doses prescribed and the brand of the vaccine. Some insurance policies cover the cost of the vaccine, too. Tata AIG MediCare Premier offers the cost of HPV after two years of continuous coverage.

Depending on individual risk factors, women may also go for mammograms to detect breast cancer as early as 40 years, progressing to annual screenings between the ages of 45 and 54 years. Regular breast self-exams can also help one become familiar with how breasts normally look and feel, thus allowing women to notice any changes that might warrant further consultation with the doctor.

Says Parthanil Ghosh, president, retail business, HDFC ERGO General Insurance: “Early detection plays a vital role in preventing and managing cancer. For cervical cancers, routine PAP smears or HPV tests can be carried out from the age of 21, resulting in swift intervention and preventing progression.”

For colorectal cancer, starting at the age of 45, screening tools like stool tests, flexible sigmoidoscopy, colonoscopy, and CT colonography (virtual colonoscopy) can aid in early detection, when treatment works best.

Plans For Protection

Are Standalone Health Insurance Policies Enough?

Treatment of critical illnesses, such as cancer can cause considerable financial strain. Hence, a health insurance policy with a small coverage would be woefully inadequate to provide coverage against cancer.

Says Bhaskar Nerurkar, head, health administration team, Bajaj Allianz General Insurance: “It is crucial to recognise the nuances in coverage, especially when dealing with severe illnesses, such as cancer. While addressing critical illnesses, standalone health policies often have limitations, as they primarily focus on hospitalisation expenses within the predetermined sum insured.”

Agrees Puri, “Conventional standalone health insurance policies cover the superficial needs of a cancer patient, as it involves the cost of

in-patient hospitalisation, surgeries, and pre-and -post hospitalisation expenses, among others.”

In the majority of cases, the coverage offered by such policies is inadequate to provide end-to-end protection. Also, these policies often have financial barricades, such as sub-limits and co-payments, which further necessitates the purchase of a separate policy in order to get wholesome coverage.

Should You Look At Specific Cancer Policies? According to Ghosh, dedicated cancer insurance policies or standalone plans designed to provide financial support in case of cancer diagnosis offer more specific and comprehensive coverage compared to riders attached to health insurance plans.

For instance, HDFC ERGO’s iCan policy covers both conventional and advanced cancer treatments along with in-patient and outpatient treatments. Besides, under this plan, one can renew the policy even after making a claim.

HDFC ERGO also offers a Cancer Plan as part of its ‘my: health Women Suraksha package.’ This plan not only covers major malignant cancers, but also provides coverage for cancers, such as cervix, uteri and breast, at the initial stage.

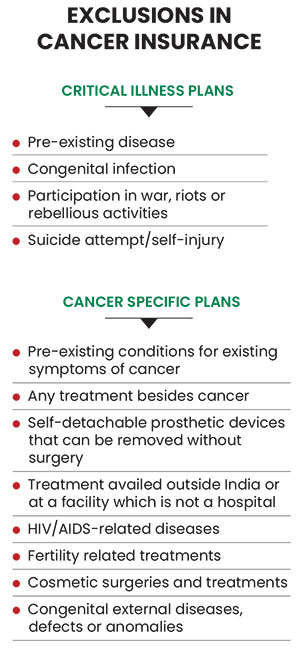

What About Critical Illness Plans? It is important to understand the difference between critical illness and cancer-specific health insurance plans. The principal difference is that critical illness policies cater to a broader spectrum of listed critical diseases, including stroke, major organ transplant, paralysis, cardiac arrest, multiple sclerosis, kidney failure, total blindness, deafness, and some life-threatening cancers, while a cancer-specific plan only covers treatment and expenses related to cancer.

While critical illness plans offer a lump sum benefit upon diagnosis, they typically cover cancer only in advanced stages, mainly when a malignant tumour exhibits uncontrolled growth and invasion into normal tissues.

Says Nerukar: “Critical illness plans do not cover complications arising from cancer, and they lack features, such as premium waivers or annual sum insured enhancements for claim-free years. Additionally, if a policyholder exhibits cancer symptoms within the initial 90 days, the stipulated waiting period in most insurance policies, the plan ceases to be in effect.”

Can Life Insurance Riders Help? One can look at critical illness riders to provide additional coverage. Critical illness riders in life and also health policies (some health insurance policies, such as one provide by HDFC ERGO do provide some cover, but it’s not so common in the industry), provide additional financial protection to policyholders in the event of a specified critical illness diagnosis, such as for cancer, heart attack, kidney ailment, paralysis, and others.

Says Nerukar: “These riders typically offer a lump sum payment upon the diagnosis of a covered critical illness, which can be used by the policyholder as needed to cover medical expenses, household bills, debt payments, and other financial obligations to maintain the quality of life during the recovery period.” For instance, 25 per cent of the sum assured may be paid on diagnosis of early-stage cancer and 100 per cent on diagnosis of some major cancer. Some policies may even waive premiums for a certain number of years on diagnosis of early-stage cancer.

A lump sum payment comes with another benefit. Dealing with cancer can be physically demanding and emotionally draining, often leading to distractions in the work life, including difficulty related to being 100 per cent fit for the duty. In some cases, individuals may be unable to continue work or may need to take extended leave from jobs to focus on treatment and recovery. To overcome this challenge, it’s essential to protect one’s income through insurance solutions, such as critical illness riders.

Says Amit Chhabra, chief business officer, health insurance, Policybazaar.com: “These riders provide a fixed lump sum income in the event of diagnosis of a critical illness, including cancer. This lump sum payment can help offset the loss of income during the treatment and recovery period, thus allowing individuals to meet their financial obligations and maintain their standard of living.”

What Should You Do? It may make sense for you to go for a combination. Says Puri, “A balanced combination of indemnity and benefit-based cancer insurance plans can provide additional financial protection beyond the ambit of a standard health insurance.”

Indemnity plans cover the wholesome needs of a customer ranging from diagnosis, treatment, surgery, recovery, prognosis, and ancillary costs, including out-of-pocket expenses. Benefit-based plans, which mostly come as riders, will help in combating other financial liabilities that may get impacted due to the onset of cancer.

On the other hand, dedicated cancer insurance policies are standalone insurance plans designed to provide financial support in case of cancer diagnosis, and offers more specific and comprehensive coverage compared to riders attached to health insurance plans. These may be beneficial for people with a family history of cancer. Typically, family history and smoking habits can increase susceptibility to cancer by influencing genetic predisposition and exposure to carcinogens.

Also, one should be careful about the sum assured as like other illnesses, cancer often requires ongoing treatment, and so, it is difficult to predict the total cost. So, even a coverage of Rs 20 lakh may not suffice.

Adds Ghosh: “It is because of this reason that insurance companies have introduced specialised cancer health insurance plans. These plans offer higher coverage limits, sometimes up to Rs 1 crore or even Rs 3 crore. Such plans can better safeguard the policyholders against the financial impact of cancer treatment.”

When cancer strikes, besides the emotional toll and mental trauma, the financial implications can hurt a lot. Proper planning will ensure that one is prepared against the disease.

meghna@outlookindia.com