It was in March 2020 that the Covid virus first started showing its true colours. Two years later, the world and the lives around us have changed in more ways than one. With Covid creating new priorities, it is not surprising that people’s life and financial goals have also changed. Unplanned medical expenditure, job losses, pay cuts and volatility in the stock markets have all played a part in how people now visualise their financial lives.

According to a recent report by Standard Chartered, Wealth Expectancy 2021: Bridging The Confidence Gap, almost 94 per cent of the Indians who participated in the study, have set new life goals in the last 18 months. The study, which was conducted across 12 global markets, interviewed 1,501 people in India. Almost 41 per cent Indians said that the pandemic prompted them to rethink their overall priorities, and 39 per cent felt it was important to make their finances future-proof.

A case in point are Sabyasachi (45) and Rashmita Mukherjee (43), who live in Kolkata with their 11-year-old son, Sourja. They are among the thousands in India whom the pandemic has stirred to change the view. “During the pandemic, I saw my friends and acquaintances losing their jobs and businesses. Some people close to me suffered from Covid and some even lost their lives. That kind of shifted my mindset towards money and investments,” says Sabyasachi, who is a chartered accountant by profession.

Realigned Priorities

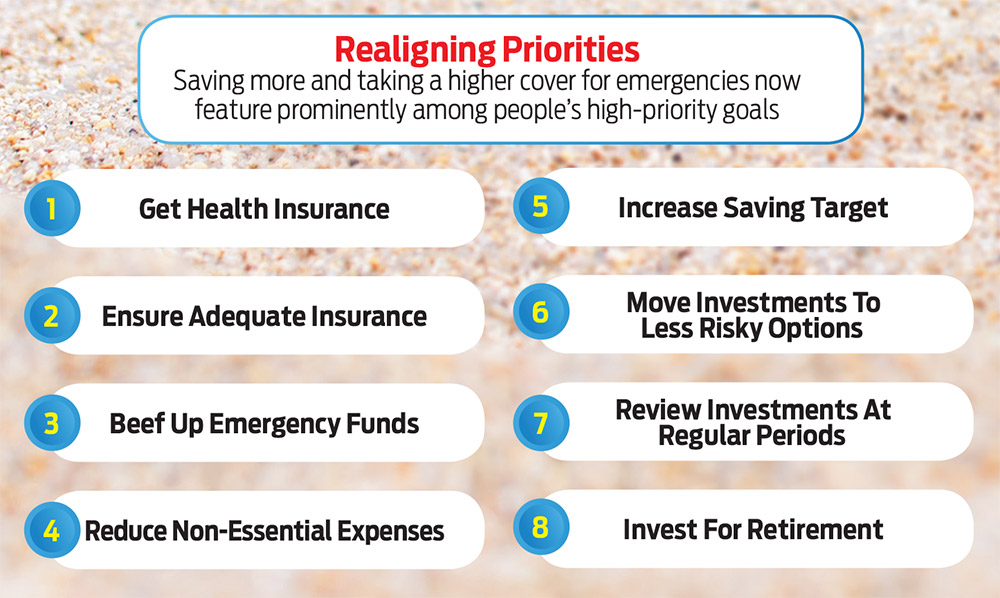

Among the major financial goals that have emerged for families post-Covid are safeguarding health, providing for the immediate future and planning for long-term goals.

Focus On Health: The pandemic was the much-needed trigger to make more people conscious of their health and the costs that medical emergencies can entail. According to the Standard Chartered report, four in 10 (42 per cent) Indians in their survey have set a new goal “to improve their health”.

“The pandemic has shown why health cover for the entire family is required and all members need reasonable cover. Remaining underinsured or uninsured has a direct implication on your overall finances,” says Harshad Chetanwala, co-founder, MyWealthGrowth.com, an online investment and research platform.

If you haven’t already done so, review your health cover to ensure adequacy. For example, after the onset of the pandemic, the Mukherjees increased the sum insured of their family health insurance from Rs 10 lakh to Rs 20 lakh.

Trimming Expenses: The pandemic seems to have turned the most spendthrift of individuals into savers. Job losses and pay cuts were realities that made people rethink their spending and saving. “We curtailed our monthly expenses, like a lot of other people. For example, we reduced spends on movies and dining out. We subscribed to OTT platforms to watch movies,” says Sabyasachi.

Redefining Risk: The pandemic affected the confidence levels of many investors, too, making them risk-averse. Almost half (48 per cent) of those polled in the Standard Chartered survey in India felt that the pandemic made them less confident about their finances.

The irregular movements in the stock market further accentuated this. “Seeing the volatility in the market, I started investing more in mutual funds. I also moved my existing mutual fund investments from risky categories to the balanced category (which invests in both debt and equity according to the market levels),” says Sabyasachi.

Getting Future-Ready

The Covid pandemic was one incident; there can be many more, and it is only prudent to be ready for them.

Provide For Emergencies: One thing that the pandemic has taught us is that it is important to provide for the immediate future so that one can tide over short-term emergencies, medical or otherwise.

For a medical emergency, having adequate health insurance is the answer. “In a formal goal-setting exercise, there is provision for health emergencies and hence no tweaking is required if already considered. What we need to remember is that a pandemic caused by just one disease can wreak havoc with your finances; there can be many other medical issues,” says Chenthil Iyer, founder and chief strategist, Horus Financial Consultants, a financial planning firm.

Build an emergency fund so that it is easier to deal with loss of employment or a pay-cut and you are mentally free to look for new avenues. Experts suggest saving a corpus amounting to six months of expenses; post the pandemic, some suggest topping this up to one year’s expenses.

Prepare For Near-Term Goals: If you do not plan for near-term goals, you may end up having to pay for them with money meant for other purposes. If your investments were in equities, you may have to bear a loss when you sell if the market is down like it was during the March-April period of 2020.

Events like a pandemic can affect not only your overall portfolio but also short-term financial goals. “To minimise the impact of such events on near-term goals, you can withdraw from the accumulated corpus every month starting six to 12 months from the goal. This will help de-risk the accumulated corpus and minimise the impact on the goal,” says Chetanwala.

Strategise For Long-Term Goals: Long-term objectives like retirement, which may be 10 or 20 years away, may not be immediately affected by an event like the pandemic and you would have sufficient time to restore the portfolio’s health. However, a pandemic-like situation can create issues for those who plan to retire in a few years’ time.

“If the retirement funds are hit, the only option is to extend the time to retirement by a few years. One can consciously change one’s risk profile and make the available investment portfolio a little more aggressive to fill the gap,” says Iyer.

To do that, one can augment the long-term investment plan by adding more whenever the cash flow permits. Investing in equity is one way to improve the chances of your investment earning higher returns. “Equity by nature is expected to be volatile in the short term and performs well over a longer period. Hence, you should invest only your long-term money in equity. Even if the market corrects in the short- or mid-term, your investment has sufficient time to regain lost ground,” says Chetanwala.

Review Regularly: Reviewing financial goals every six months to a year can help you manage asset allocation and remain focused on goal-based investing. “You can check the status of investments mapped to different financial goals. You may need to take necessary action to maintain the asset allocation and even try to take advantage of market movement,” says Chetanwala.

If you need to redirect some of the investments, do so without disturbing your overall portfolio. “One way to do this is to redirect the new and subsequent investments into the avenue you want to invest in. This can work well when you plan to rebalance your asset allocation,” says Chetanwala.

While the pandemic may have led you to reset some of your life goals, remember that there will be other tough situations in the future. However, if you plan your finances properly, you will be able to ride out any storm whenever it hits.

***

Adjusting To New Risks

According to a recent report by Standard Chartered, Covid has prompted many people to set new life goals

97% have taken at least one action relating to finances last year

94% set new life goals in the last 18 months

41% said they need to adapt finances to economic situation (market volatility, low interest rates, etc.)

39% felt it is important to future-proof finances

The study was conducted across 1,501 Indians

meghna@outlookindia.com