The hefty text on any investment memorandum runs through hundreds of pages, often frustrating the reader, and creating confusion. Even investment czar Warren Buffett once slammed the system, saying it was humanly impossible for an investor to go through 700 or 800 pages of regulatory compliance before taking an informed decision to invest in the securities market.

“It’s a perennial problem for an investor,” says Sandeep Shah, Senior Partner at NA Shah Associates, “There are too many compliance protocols for the investor to comprehend. And, eventually, it leads to utter confusion.”

The need for a change in the age-old system has finally pushed the Indian securities markets to take a big leap towards ease of doing investment. And, the markets regulator Securities and Exchange Board of India (Sebi) has geared up to introduce the concept of Accredited Investor (AI).

The Accredited Investors will be there alongside their existing peers like retail investors, high net-worth individuals (HNI) and institutional investors, who are classified based on their investment exposure and risk appetite.

An Accredited Investor represents a class of people who have an understanding of various financial products and the risks and returns associated with them and, therefore, they are able to take informed decisions regarding their investments. Although the concept of AI is about to debut in India, this well-established class of investors is active in various developed jurisdictions and are recognised by many securities and financial market regulators around the globe.

AIs have contributed immensely to the growth of various markets where they have operated. While name Accredited Investors was coined in the US, this class of investors are called Experienced Investors (EIs) in the European Union and the UK. Private capital offering is a huge market as not all issuances of securities are listed on floor of exchange. AI or EI participate in all kinds of investments and not necessarily in debt market.

AIs are an evolved group, as they need prior accreditation based on certain stringent criteria. Sebi-registered MFs are a classic example which have to follow stringent conditions as they are pooled investment vehicles.

Sebi has floated a concept paper on the subject, which says AIs are considered to be informed investors on the premise that their financial capacity – which is generally ascertained from their income and net worth – enables them to hire expert managers or advisors as required. Certain jurisdictions have also attempted to consider the knowledge and investment experience of the investor as one of the qualifying criteria to be an AI, alongside financial capacity. It is also considered that their financial capacity gives them an edge to absorb loss and so relatively higher-risk products may also be suitable for such investors.

“The category of AIs is the need of the hour. They are sophisticated enough to not require extensive regulatory protection, and therefore, issuers of securities and providers of financial/securities market products/services are offered a regulation-light regime, to offer their products/services to AIs. This sometimes implies relaxation with respect to disclosure requirements, filing of offer documents, prospectus etc, and flexibility in respect of investor reporting,” says Uttara Kolhatkar, Partner, J Saga Associates, which specialises in securities markets law. Once the AI regime is in place in the country, the question that arise is what will be the fate of retail investors who form the big chunk of the market, particularly in India.

According to Shah, the AI category will help the issuers of various types/format of capital instruments which are not approved by regulators to retail investors. “This reduces the backlash on the regulator for not monitoring the issuers of capital and leading to un-savvy investors losing money. The retail investors will have to get satisfied with capital offering which is more regulated like mutual funds, listed shares, etc,” he says. Kolhatkar is more optimistic about the fate of retail investors. She says there will be a market for retail investors as well due to the IPO regulations, which mandate a percentage to be allocated to retail investors. “Retail investors form a very important category of investors for equity and debt investment.”

One would wonder that as the number of disclosures will be lesser in the regulation-light regime for AIs, how an informed decision could be taken to opt for a product or services offered to them. The experts believe that the AIs make a well-informed class of investors, and can take an informed decision even with limited disclosure standards.

“Introduction of diverse structured products to cater to AI investment choices will be an important step, and AIs with a precondition of accreditation will act as a safer set of investors. This will contribute to improving the regime and increase general confidence of investors and investees,” Kolhatkar says.

Certain jurisdictions also permit issuers or providers of financial or securities market products or services to design and offer products and services exclusively to AIs. Having AIs also signifies an evolving and progressive capital markets regime.

Sebi regulates various investment products and services offered by market intermediaries like stock brokers, mutual funds (MFs), portfolio management services (PMS), Real Estate Investment Trusts (REITs), Infrastructure Investment Trusts (InvITs), Alternative Investment Funds (AIFs) and Investment Advisory Services offered to various category of investors. The investment products and services are distributed through different distributors of the financial products. Very often these distributors mis-sell these products to targeted investors, where there is a complete mismatch between the goal of the investor and the return offered by such products. In order to avoid such mismatch and protect investors’ interest, the watchdog has prescribed one common measure to stipulate a minimum investment threshold for each regulated product and service.

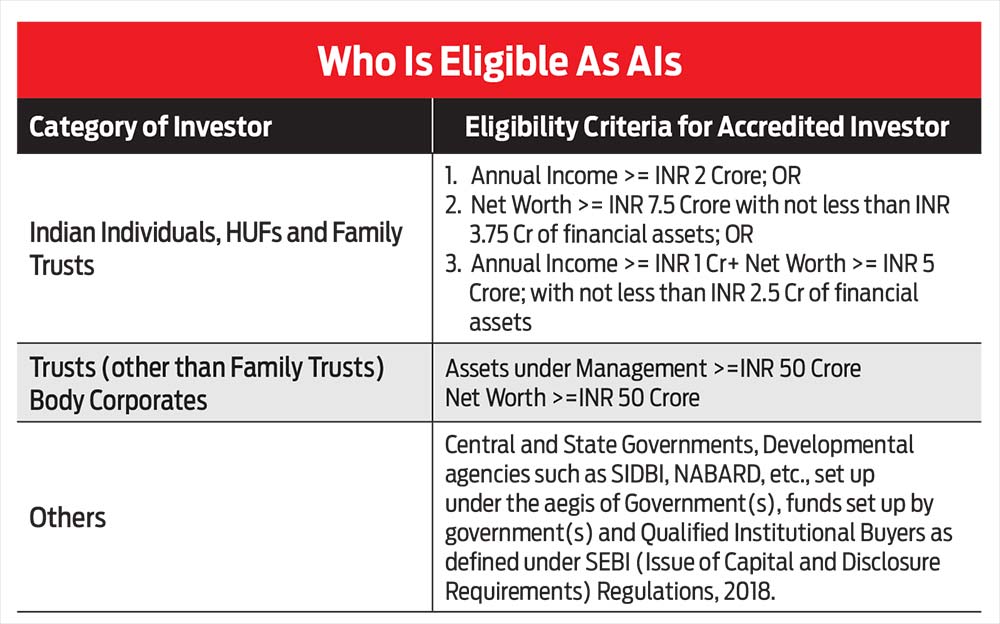

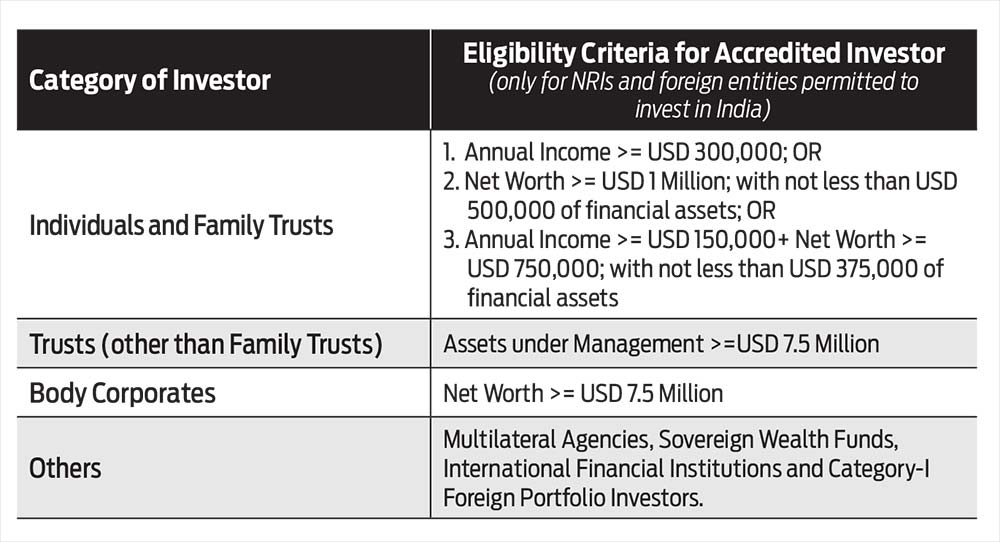

Sebi says there is a case to consider introduction of the concept of AIs in the Indian securities market. It is envisaged that the introduction of the concept of AIs with uniform eligibility criteria, accompanied with a flexible regulatory framework for the various products and services may be beneficial to the Indian securities market. It has also prescribed eligibility criteria for various categories of investors who can be termed as AIs.

In the international debt markets, especially the bond markets, AIs play a very active role and are an evolved lot of investors who invest in Reg S and Rule 144A Bonds (of Securities Exchange Commission, SEC, US market regulator) regularly and are very savvy and well-informed to take an informed decision on investing in Indian debt paper or instruments.

The regulatory light regime for AIs will also help Indian authorities to develop the domestic debt market which is at a nascent stage. It comprises corporate bonds, government securities with AIs having international exposure. With Union government lining up a larger monetisation pipeline for its infrastructure spending, these set of international investors will play crucial role going ahead, experts said.

However, the regulator will have to exercise caution while opening the door for AI regime. “Non-AIs may be marginalised due to increasing importance given to AIs and less complex products may lose investor favour. Individual investors who do not meet specific income or net worth tests, regardless of their financial sophistication, will be denied the opportunity to invest in multifaceted markets,” says Kolhatkar.

The introduction of a regulatory light regime will call for a more vigilant markets watchdog. Preventing investor frauds is the biggest threat to Sebi at this moment as the authorities ease the investment procedure. The regulator needs to lay down stringent procedures and licences in place to meet the AI requirements. It should frame suitable guidelines to manage and control AI and put in place defined measures of professional knowledge, experience or certifications in addition to the existing tests for income or net worth to qualify as AI. “One of the major challenges for the regulator will be to have clarity on the issue of net-worth. The success of the concept paper will majorly depend on how the regulator defines the net-worth criteria for various categories of investors,” says Shah.

According to him, Sebi will be required to define clearly what is the market value of investment, what are illiquid stocks, whether they will form the part of the net-worth or not to arrive at the net-worth of an individual investor to qualify as AI.

To classify Non-Resident Indian (NRIs) as AIs would be a tough task for the regulator as NRIs usually avoid to show and share details of their international accounts. “The regulator will have to bring in practicality while framing the eligibility criteria of various categories of investors to be recognised as AIs. The major task of the regulator will be to arrive at what goes into the basis of net-worth computation,” says Shah. Some other classes of investors, however, fear of being side-lined and the AIs being given the first preference in majority of products and services. Kolhatkar argues that since the Indian capital market is evolving and to keep up with the global challenges, it is time to introduce AIs as a sophisticated category of investors. The other categories of investors are equally important to enable diversification of portfolio for investment purposes, and their importance may not necessarily get diluted. After all, the main function of a market regulator is investor protection – to protect the rights of investors and ensuring safety to their investments.

“Retail investors will continue to retain their important place in the Indian capital market as in a market, there is a specific role which typically every category of investor plays,” she says.

yagnesh@outlookindia.com