When it comes to taking credit, consumers are spoilt for choice these days. Loans and credit cards have been relegated to the quintessential realm, with new-age options like buy-now-pay-later (BNPL) schemes taking the market by storm. While BNPL schemes bring convenience to the table, they are also riddled with risks for indisciplined borrowers in terms of high interest cost.

The market for credit is growing. According to a report named A Review of India’s Credit Ecosystem, released in June 2021 by Experian, a global information services company, and Invest India, an agency for investment and facilitation, India’s credit ecosystem remains resilient despite the pandemic.

“Today, in India, there are 35 million customers having about 60 million credit cards. But there are about 190 million Indians on one credit bureau itself. The 35 million customers will grow to 100 million in the next five-six years; 60 million cards will go up to 200 million cards over the same period. This massive opportunity and growth are going to be led both by credit cards and BNPL. In the credit industry, 1 million customers are worth a billion dollars in market cap,” says Prateek Jindal, co-founder and chief product officer, Uni Cards, a BNPL firm.

Considering its growing popularity among the Gen-Z and the millennials, BNPL is being touted as the next big thing in online payments. “BNPL will be key in bringing the next 100 million users into the credit card or equivalent industry. Many banks, NBFCs (non-bank financial companies) and fintech firms are embracing BNPL as it brings innovation and offers great customer experience. Moreover, innovation in technology such as artificial intelligence and machine learning has made it possible for financial institutions to reduce the risk of fraud and defaults,” says Jindal.

While BNPL is creating a lot of buzz, there are other loan products as well in the market, such as credit cards and EMI cards, and it’s important to understand their models, risks and advantages.

The BNPL Model

BNPL, the latest entrant in the credit space, has become popular because it allows immediate access to credit even for small-ticket purchases and, typically, without the need to go through any paperwork or documentation.

The concept of BNPL was introduced by fintech platforms such as Simpl, ZestMoney, LazyPay, Flexmoney, Paytm Postpaid and Amazon Pay Later. While some offer an online credit limit to make purchases from their website alone (such as Amazon, Big Basket or Flipkart), other fintech platforms like ZestMoney or Paytm Postpaid allow purchases through other websites as well. Then, there are some fintech platforms, including EarlySalary, KreditBee and Uni Cards, which also offer a card with instant credit facility. Even banks such as ICICI Bank, HDFC Bank and Axis Bank have forayed into this space.

How Does It Work? The broader features of BNPL are the same as credit cards. “Just as in the case of credit cards, consumers opting for BNPL schemes have to repay by a pre-specified date. Interest is levied only on failing to repay for the transaction by the pre-specified date,” says Gaurav Aggarwal, senior director, Paisabazaar.com, an online marketplace.

As it is with credit cards, consumers can opt for the EMI facility with BNPL too. Interest cost may be levied or waived off on opting for the EMI facility, depending on the tie-up between the lender/retail platform and the merchant/producer of the goods/services. Some BNPL merchant tie-ups may also come with additional discounts or cashback offers, just as in the case of zero-cost EMIs available through credit or debit cards. “BNPL facilities can act as an alternative for consumers, whether they have or don’t have credit cards,” says Aggarwal.

The BNPL model allows you to pay for an item over a period of one month to three years, depending on the price of the item and the credit provider. Simply select the Pay Later option from the different modes of payment and the first payment will either start from the next or the subsequent month.

How Much Can You Borrow? The biggest attraction of BNPL schemes is the small-ticket size. ICICI Bank’s PayLater, for example, is a digital credit facility for small payments. “The facility enhances the usability designed for young customers in the age bracket of 25-30 years. Typically, they are new to credit and require a digital credit facility for small-ticket items. We have seen customers using PayLater by scanning a QR code at a local outlet, for bill payments, internet banking or paying online merchants. A large number of our customers use this for their small-ticket, high-frequency transactions to avoid such transactions getting reflected in their bank statement. Customers receive real-time approval and don’t have to deal with cumbersome paperwork,” says a spokesperson from ICICI Bank.

The amount you can borrow using BNPL depends on the lender. For example, at Amazon Pay Later, the minimum purchase amount is Rs 3,000, which is to be repaid over three to 12 months. ZestMoney, a fintech platform, allows consumers to repay in three to four EMIs at no interest.

EarlySalary card allows users to set a credit limit and the minimum transaction amount is Rs 3,000. However, consumers can convert any transaction above Rs 500 into three to 12 EMIs.

Convenience And Benefits: What attracts users to BNPL is the convenience. For example, EarlySalary issues its SalaryCard within a day, without any paperwork. “SalaryCard, which is powered by Rupay, helps users make instant purchases with online merchants like Flipkart and Amazon without worrying about the current budget constraints,” says Akshay Mehrotra, co-founder and CEO, EarlySalary.

There are other benefits as well. “Reward programmes for credit cards are common. Banks earn higher profits through them (credit cards) and give lucrative rewards to encourage consumers to use the cards more often. But through SalaryCard, the consumer can get cashback on every transaction. Our data shows that millennials opt for SalaryCard over credit cards, as it is tougher to get a credit card. We also offer a zero-touch digital solution with no hassle of maintaining a physical card, which is beneficial during times such as the pandemic,” says Mehrotra.

High Cost And Risks

BNPL is convenient but can be risky, especially for indisciplined borrowers. The ticket sizes for most BNPL purchases are usually small enough to create the illusion of having low debt, but when ignored, it can cost the borrower dear.

For instance, HDFC Bank levies an annual interest rate of 28 per cent (2.33 per cent per month) on BNPL, which can go up to 42 per cent, depending on the customer’s credit history. Most fintech platforms charge 28-30 per cent annually. At Uni Cards, if you convert a bill into longer-tenure EMI, an interest rate of 14-18 per cent is applied. In Pay 1/3rd Card, the minimum due has to be paid every billing cycle; else there is a late fee.

If you buy something for, say, Rs 500 at a 27 per cent annual rate or 2.25 per cent per month, the interest you would pay each month would be around Rs 11.25. However, if you forget to pay the minimum due amount by the due date, the cost, including late fee (which can be Rs 100 for outstanding up to Rs 500) and interest rate may balloon to Rs 110.56. Simply put, the item will cost you not Rs 500 but Rs 610.56, a rise of more than 22 per cent.

“Before you opt for BNPL, it is recommended that you read and consider the terms and conditions. You should also be aware that BNPL is a financial product similar to a credit card and it is crucial to have a disciplined approach to repayment, ensuring it is done within the stipulated due date. In case of a default or missed payment, your credit score will be affected, thereby reducing your chances to get a new credit line or loan in the future. It is advisable to ensure timely repayments even on these new-age credit options to enjoy their benefits in the long term,” says Navin Chandani, managing director and CEO of credit bureau CRIF High Mark.

To avoid getting caught in the loop of ever-increasing interests and penalties, assess your repayment capacity before taking any credit, be it through a credit card or a BNPL scheme. “Consumers should factor in their repayment capacity while using BNPL mode or credit cards. Failing to repay for the transactions by their due date can cost them hefty penal interest charges and/or late payment while adversely impacting their credit score. Those who lack the capacity to repay the entire transaction amount by the next bill due date should opt for EMI facilities as per their repayment capacity,” says Aggarwal.

How Does It Compare?

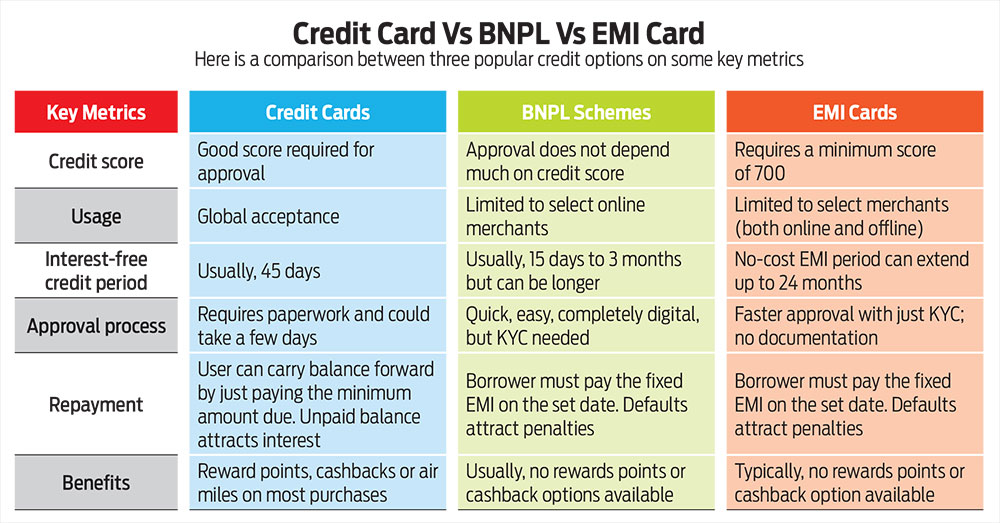

Credit cards, EMI cards and BNPL products have many common features and some that differ. Understand the nuances of each to make an informed choice and make the best use of the different facilities they offer (see Credit Card Vs BNPL Vs EMI Card).

Interest-free period: As of now, BNPL provides the longest interest-free period of up to three months. For instance, Uni Cards’s Pay 1/3rd card offers an interest-free credit period of up to 90 days. This is a zero-balance pre-paid Visa card. But all don’t offer long interest-free periods, which can be as short as 15 days also. In comparison, credit cards, typically, provide an interest-free period of 45 days. EMI cards allow you to settle your credit through EMIs over a fixed period of time, which varies. This is also known as the No-Cost EMI option that most physical stores offer.

Offers: Credit cards offer reward points that can be used for subsequent purchases, as per the card’s policy. “Some card issuers also allow their users to redeem their accumulated reward points for paying off their credit card bills,” says Aggarwal. However, the reward points are, typically, revoked if you opt for the credit card EMI facility.

“Consumers should carefully compare the various cashback or discount offers available on goods or services to be purchased through BNPL schemes and credit or debit cards. They should opt for the mode that costs them the least interest and/or earn the highest discount/cashback on the transactions,” says Aggarwal.

Availability: Credit cards are widely accepted, for offline as well as online purchases. EMI cards—first launched by Bajaj Finance in 2012, followed by EMI on debit cards by ICICI Bank, and others including HDFC Bank and Tata Capital—are mostly availed of on consumer durables. However, the facility, both online and offline, is available only with select merchants. BNPL, too, is at present offered by select online and offline merchants.

There is a lot of choice available in short-term small-ticket loans. Lack of credit history is no longer a deterrent for small loans. However, each of the products described above—credit cards, EMI cards and BNPL—is a loan and should be treated as such.

The way to make the best use of these is to take credit as per your repaying ability. Avoid impulse buying, and pay back on time.

***

BNPL

The new kid on the credit block

What Works

- Integrated with online stores’ checkout page, which makes it easier to use

- Increases the affordability level with immediate access to credit

- Quick and convenient setup; completely digital; instant approval

- Interest-free options available; no setup fee

- Does not require high credit score for approval

- Flexible re-payment; option to pay in EMIs

What Doesn’t

- Not accepted universally

- Higher late fees charged as a penalty for late payments; payment date not negotiable

- Lower credit limit based on credit history

- Encourages high-impulse purchases

- Late payments or missed payments hurt credit score

- It’s a loan and, hence, outstanding cannot be revolved even when there is cash crunch

***

CREDIT CARDS

Among the traditional credit products

What Works

- Help build a healthy credit rating when dues are paid on time

- Interest-free credit period for up to 45 days

- Get rewards for eligible purchases and redeem them on specified items

- Offer protection against fraudulent usage

- Allow users to keep track of expenses

- Can be used for purchases, both at the point of sale and online

What Doesn’t

- Late or missed payments or paying just the minimum amount due can hit your credit score

- Interest rates range from 2.5-3.5% per month for revolving credit, which is quite high

- Using too much credit (credit utilisation ratio) or repeatedly applying for cards affects your credit score

- Carrying forward outstanding balance every month can create a debt trap

- Have too many terms and conditions, which can be confusing

- Growing cyber security issues make credit cards vulnerable to attacks

***

EMI CARDS

An in-between product

What Works

- Allow users to pay in full within the selected tenure (minimum 3 months)

- Offer no-cost credit

- Payments get debited from bank account each month

- Can be used with major online merchants and physical outlets

What Doesn’t

- Do not allow carrying forward outstanding balance even if you are short on cash. Defaults attract penalties

- Do not offer rewards, cashbacks or points

- No online payment option

- Not accepted globally or everywhere in India

The author is a Freelance Writer