Saving up for the higher education needs of their child, is undoubtedly, an important task for many parents.

Planning for higher education means carefully allocating money for this purpose over several years, at least 7-8 years, taking into account rising inflation, the course in mind, the university, the city – local or foreign, living expenses, and numerous other expenses.

This entire process could throw your financial life into a tizzy, if not planned ahead properly.

Here are three ways in which you could save around Rs 70-80 lakh in the coming decade for your child’s higher education studies.

Try to start investing early: There is a popular saying: “It is best to start investing earlier in small increments rather than invest big sums at a later date.” The typical age for higher studies or foreign studies in India is once the child turns 18. Suppose your child is 10 years old now, you still have 7-8 years to save the money.

“You can use this period to invest in instruments that yield better returns, i.e., equity instruments such as stocks, mutual funds, and so on. You can invest in a way that your investment matures when your child turns 18. Investing early will provide you the benefit of compounding as well,” says Anup Bansal, chief investment officer, Scripbox, a wealth management firm.

You can build the corpus in three ways.

1. Keep a lump sum aside so that the money grows to the required corpus. Assuming 10 per cent annualised return, you would need around Rs 37 lakh to grow it to Rs 80 lakh in eight years

2. Invest a fixed amount regularly to generate the corpus. You would need to invest around Rs 60,000 every month for the next eight years to grow it to Rs 80 lakh, if the annualised return is 10 per cent per annum.

3. Start with a smaller lump sum and invest regularly. The regular investment amount will depend on the initial lump sum. For example, if you start with a lump sum of Rs 10 lakh, then you would need to invest around Rs 43,000 every month to grow it to Rs 80 lakh in eight years.

Choose suitable investment options: Where you invest your money is crucial in achieving the financial goals for your child’s future.

“You need to consider the rising inflation levels before investing. Equity investments yield better against inflation compared to fixed income tools, such as a bank fixed deposit (FD) or savings account. The average return for equity instruments is around 12 per cent, while for a bank FD, it is merely around 5-6 per cent,” says Bansal.

The key is to create a risk-adjusted portfolio, and for that, diversification is the key. It is better to consult a portfolio advisor or manager to identify the exact investment match for your child’s higher education needs.

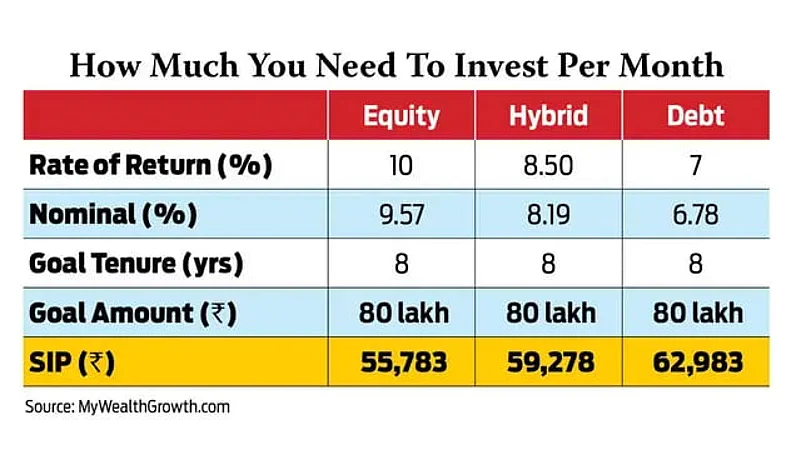

“It is ideal to invest in diversified equity funds, where the time horizon is of 7-8 years. You need to invest approximately Rs 55,000 per month for the coming eight years to reach the goal of Rs 80 lakh, considering a 10 per cent per annum return. Equity has the potential to generate better returns than any other asset classes for the time horizon of the goal,” says Harshad Chetanwala, co-founder, MyWealthGrowth.com, an online mutual fund investment platform.

You could invest in a blend of large-cap, flexicap, and large- and mid-cap equity funds.

“Those with moderate risk appetite can try to invest partially in balanced advantage funds along with equity funds. This will help them to reduce risk and volatility, but it can lead to an increase in the monthly investment amount to Rs 60,000, if we assume a return of 8.5 per cent per annum from this hybrid portfolio,” says Chetanwala.

Investment in debt funds: If someone wants to build the corpus using debt investment, they can consider investing in debt funds, like banking and PSU debt funds, corporate bond funds, and dynamic bond funds. In such a case, they will have to invest nearly Rs 63,000 every month, as their return would be around 7 per cent per annum.