Low home insurance adoption could be probably due to attention bias, which refers to our tendency to give greater importance to things that catch our attention and less to matters that are hidden. While this bias can be helpful sometimes, it can lead us to ignore important decisions, such as purchasing home insurance.

Home insurance is often overlooked, even though a home typically represents a larger share of one’s wealth compared to, say, a car. This may be because the risks that threaten a home, such as natural disasters and human errors, are not perceived as imminent.

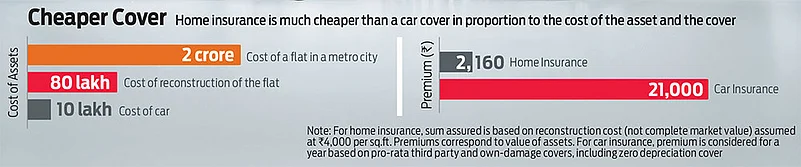

Contrast this to car insurance, whose penetration is much higher because while driving in the city traffic, the possibility of someone bumping into your car is immediate and real. So, people have a higher appreciation for risks faced by their car and are comfortable paying hefty car insurance premiums every year.

However, risks from natural disasters are equally real, and a home insurance policy can protect against them. Many parts of the country, whether it is Chennai, Uttrakhand, Gujarat or Delhi, are prone to floods and earthquakes. These events can cause significant personal and material loss, and their frequency has been increasing due to rapid climate change.

In addition to natural disasters, homes are vulnerable to human errors, such as fires caused by live cigarette butts, short-circuited air conditioners, gas leaks and pipe bursts. Rare but devastating events, such as terrorist attacks or aircraft crashing into a house, are also potential risks.

The Insurance Regulatory and Development Authority of India (Irdai) has made efforts to simplify home insurance with the introduction of the Bharat Griha Raksha product, which is offered by all general insurers. There are three standout features of this product.

First, there is an under-insurance waiver. Typically, in property insurance, you are required to declare the estimated cost of reconstructing the building. If the actual cost of rebuilding the entire structure is higher at the time of loss, claims may be reduced proportionately. Determining the correct sum assured requires expertise that many homeowners may not have.

The under-insurance waiver ensures that you are indemnified up to the value of the sum assured, regardless of what the correct sum assured should have been. There will not be any deductions for under-insurance, and the insurer’s maximum liability is capped at the total sum assured.

Second, several coverages that had to be specifically requested by the policyholder in the past are now automatically included. For example, all policies are insured on a reinstatement basis, and earthquake coverage is automatically included. This significantly reduces the burden on the policyholder to understand the policy’s inclusions and exclusions.

Third, some definitions within the policy wording are very specific. For instance, the home building is considered to include sanitary fittings, electrical wiring, the garage, domestic outbuildings, compound walls, fences, gates, internal roads, and air conditioning systems. This removes the substantial insurance compliance burden on the policyholder. In the past, many policyholders would just declare a lump sum without breaking it down, which could cause issues with the loss adjuster at the time of a claim. Now, such ambiguities are removed.

There are some in the industry who advocate making home insurance mandatory, similar to the third-party liability component of car insurance. It is believed that many people only purchase the optional own-damage component of car insurance because they are unaware that it is optional.

However, I disagree with this view. I have seen policyholders actively negotiate with multiple agents because they know the premium for the optional portion varies among insurers, while the premium for the statutory part is fixed. If compliance was the only concern, bargain hunters would only limit themselves to the statutory part.

It is the higher awareness that has driven the adoption of comprehensive car insurance. The new home insurance product is extremely policyholder-friendly. It is yet to gain widespread attention, but there are many good reasons to purchase it.

The writer is Co-Founder, SecureNow