1 January 2026

Get the latest issue of Outlook Money

Life insurance is a critical financial tool that provides peace of mind and financial security to both the policyholder and their dependants. One of the primary reasons why life insurance is important is its ability to offer a safety net to the family in the event of the policyholder’s untimely demise. Losing a loved one is already emotionally devastating, and during such challenging times, having the financial burden alleviated can make a significant difference.

Additionally, life insurance can help secure a family’s long-term financial goals. For instance, it can fund future education expenses for children, supplement retirement income for the surviving spouse, or even act as an inheritance for future generations. Aside from providing financial security, life insurance also offers certain tax benefits.

Additionally, life insurance can help secure a family’s long-term financial goals. For instance, it can fund future education expenses for children, supplement retirement income for the surviving spouse, or even act as an inheritance for future generations. Aside from providing financial security, life insurance also offers certain tax benefits.

A robust life insurance policy is the first brick of the consumer’s financial planning foundation. There are various types of policies that offer definite returns to fulfil financial goals, safeguard retirement plans and assure a regular stream of income even during risky times.

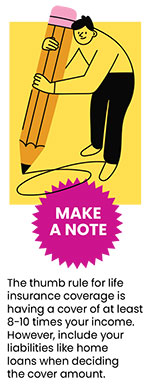

Your life insurance purchase could change depending on your life stage. The coverage depends on various factors, such as objective, income, and the needs of your dependents or any other financial obligation. However, an ideal life insurance cover should be 8-10 times of your annual salary.

Life insurers are continually innovating to provide diverse solutions. Asset allocation in unit-linked life insurance plans (Ulips) enables customers to choose multiple investment options according to their investment objective. They can invest in a mix of equities, debt, and other assets, thus offering potential growth along with the life insurance coverage.

The allure of asset allocation lies in its capacity to customise investment portfolios according to individual risk appetites and aspirations. For those inclined toward higher growth potential, allocating a portion of investments to equities can harness the volatility of the market to yield substantial returns over the long term. Conversely, a conservative investor may opt for a higher allocation in debt instruments, prioritising stability and capital preservation.

By integrating investment diversity and life insurance, policyholders can achieve a multifaceted spectrum of benefits. Not only does this approach foster potential wealth accumulation over time, but it also provides an invaluable safety net for loved ones in times of uncertainty.

The author is the MD & CEO of Aditya Birla Sun Life Insurance.