More than five years ago, when demonetisation clamped down on household cash, one of the less talked-about segments that was hit hard was women, the traditional savers. Until then, a lot of homemakers would run the ship on a tight budget and squirrel away something every month into a kitty they could call their own or have the satisfaction of whipping up during family emergencies.

The new-age homemakers have gone a step ahead by taking household finances and investments in their own hands. These new fund managers are taking charge of family money and turning cliches on their heads. Husbands earn and homemaker-turned-fund-managers save and invest.

Latest data available with the World Bank shows women constitute only 20.3 per cent (as of 2019) of the labour force in India, but when it comes to household work, women’s participation is a phenomenal 81.2 per cent daily, according to a 2019 National Sample Survey Office survey in India that covered 1.39 lakh households and 4.47 lakh people.

In a country where a large population of married women are homemakers, some are slaying it, but others may need a friendly nudge from within families.

Meet The Fund Managers

Kolkata-based Meenakshi Kochar, who has never worked a job herself, saw her husband relying on others in money matters. This eventually led her to come out of her comfort zone and take financial matters in her own hands. “I overcame my mental barrier that women can’t deal with finances. Incidentally, during the same time I happened to attend a financial literacy session that changed my life,” says the 41-year-old, who does not have formal training in finance. Meenakshi went on to join a paid financial literacy course to improve her understanding of financial concepts and products.

Delhi-based Sujata Mudgill Dargan, 39, not only manages her family’s money but also earns from the stock market. When she left her job with a travel company in 2017, she knew what she had to do—make money from the stock market. “Unavoidable circumstances forced me to leave my job, but I was sure that I won’t risk my financial independence. I immediately got my demat account activated and started building a stock portfolio,” she says.

Sujata plays the momentum in news-linked stocks to make a profit, which she uses for personal expenses. She also has a long-term portfolio of quality stocks. “Sometimes I earn enough in short-term bets to channelise the profits into mutual funds,” she says.

Photo by: Sandipan Chatterjee

Meenakshi Kochar

Meenakshi is in charge of her family’s finances. Her husband was doing this earlier, but now all he has to do is transfer funds to her bank account for household expenses and investments.

It all started when Meenakshi decided to overcome her hesitation in dealing with finances and signed up for a paid financial literacy workshop that clarified a lot of misconceptions she had about the investment world. For instance, she learnt that the high-premium insurance policies they had would provide very little return or death cover. So, she surrendered all the expensive policies they had and opted for a term plan and a health insurance plan instead. “I learned about insurance, index funds and direct mutual funds. I learnt to calculate the future values of my existing goals. This is how I started goal-based investing for my child’s (14-year-old son) foreign education, our family vacations and our retirement,” she says.

What about her own expenses? “I charge my husband for my financial services,” she says.

Money Tip: Investments are not difficult at all. If I could do it, anyone can.

Both Malaysia-based Vareen Gadhoke Ray, 41, and Apoorva B. Ashok, 32, who lives in Bengaluru, knew that it was critical to invest in a planned way and encouraged their husbands to get serious about investment planning.

Vareen decided to shoulder the responsibility as she was conversant with financial products and concepts. Now, she periodically mails her husband an Excel sheet that contains details of their ongoing investments, their value and key passwords and data. “I do it because in case something happens to me, he will have a ready-reckoner of our finances,” she says.

Apoorva and her husband were on the same page that they needed to invest in financial planning. “Realising that we would benefit from expert help, we decided to seek a financial planner’s support,” she says. The couple now goes to the planner once a year for a portfolio review. Apoorva has educated herself on various financial concepts from Facebook groups and other sources. One of the things she has learnt is that investors can also use direct plans to invest in mutual funds. “We are invested in regular plans. Now that I know about direct plans, we are willing to switch to DIY investing.”

A Long Way To Go

It is a welcome change that women are taking the reins in money matters but one cannot ignore the sad reality that even a lot of working women depend on their husbands, fathers or brothers for their taxes and investments. “When I tell women around me to ensure that their husbands buy a term insurance plan, they say they don’t want to even think about a life without their partner. If you find it hard to even imagine such a scenario, then how would you manage if it actually happens? Covid has showcased the fragility of our lives,” says Apoorva.

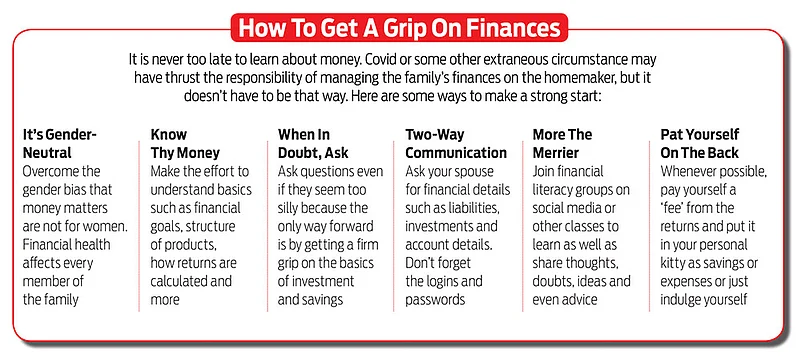

There is a growing need for women, especially homemakers, to be more financially aware. But how does one go about doing this? There is no dearth of women-specific products in the market, including financial workshops focused on women. The challenge is not limited to information; it’s bigger.

Of more concern than lack of awareness is lack of decision-making power among women. Even family members, including the elder women members, do not have confidence in the younger women. “I avoid pitching products to or conducting workshops for women because I know they are not the decision-makers at home,” says a financial planner who didn’t wish to be named.

Priti Rathi Gupta, founder of investment platform LXME, which is meant specifically for women, has had similar experiences. “I used to often conduct literacy campaigns for women employees in different organisations. They would get excited initially but that would fade within a day or two. So, now we conduct Financial Fitness Bootcamps, which have a clear call to action. This way, the learning is applied with more confidence and security,” says Gupta.

“We have all types of products, but we see that many of our women investors show a preference for products such as index funds based on their risk appetite, and gold mutual funds and sovereign gold bonds that suit their need to invest in gold,” she says.

A specific platform is as important as building an exclusive community of women investors. “I have seen that women need a safe space where they can ask questions without being judged. For example, homemakers may want to help their parents financially, but may hesitate discussing it with their husbands or in-laws,” says Gupta.

The Facebook community, Being LXME, is one such platform where women can ask their money queries anonymously or directly. “We have 22,000-plus members on the platform and experienced women are prompt in replying to the queries.”

It All Starts At Home

When Vareen was young, her father would send her to the nearby bank to withdraw money, write cheques or start a fixed deposit. “I was not scared of going to the bank or filling up financial forms, unlike other girls of my age,” she says.

But this is more an exception than the norm in most families, where boys are entrusted with outdoor tasks while girls are trained in household chores. “You cannot blame homemakers for not taking an interest in finance. This is how it is. When men are leading the finances, they will have to step up and get women involved in money decisions. Only 17 per cent viewers of my channel are women while the rest are men. The number has only marginally improved from 12 per cent last year,” says popular YouTuber Rachana Ranade, who is a chartered accountant by profession.

Photo by: Hardik Chhabra

Sujata Mudgill Dargan

Sujata got interested in the stock market during the dotcom bubble around 1990 when most of her colleagues and friends would talk about the internet bubble and the Y2K wave. “(At the time), a lot of my friends opened their demat accounts, but I wasn’t confident enough about it, so I didn’t open one. I consciously decided to pursue stock market investing only after my marriage when I became serious about savings,” she says.

Sujata’s husband was equally conscious about financial planning but did not explore beyond fixed deposits, Public Provident Fund (PPF), insurance plans or real estate. “I knew that real wealth creation lies in the stock market. I started learning about it. Not only do I invest directly in stocks but also in mutual funds every now and then.” Sujata also convinced her husband to start systematic investment plans (SIPs) in index funds. The couple now has a portfolio that is well-diversified across equities, fixed income, gold and real estate.

Money Tip: Take interest in money matters and discuss it with your spouse. It is as important as any other family matter.

On her channel, Ranade calls out to the men to get their sisters or wives to watch her videos. Sharing her own experience, Ranade says her brother and her boyfriend (now husband) encouraged her to learn more about the stock market. “If I didn’t have a positive surrounding, I would have never reached where I am today.”

Ultimately, women-oriented financial products or a specific pitch has limited traction; it is the family that needs to build an enabling environment where women are treated on a par and their financial and other decisions are trusted.

Familial support can go a long way in how homemakers manage their money. The crisp Rs 500 and Rs 1,000 currency notes that women pulled out from hiding places during demonetisation could have easily grown into a corpus if the savers had known where and how to invest.

The good news is that some homemakers have already donned the fund manager hat at homes; others just need to follow suit.

***

For Women Only

The financial industry has not ignored women. Almost all lenders offer concession up to 10 basis points on home loan rates to women. While homemakers cannot apply for a loan due to lack of a regular income, they can be co-owners. Having a woman co-owner has multiple benefits such as concession on stamp duty and sharing the tax burden.

More recently, specific health insurance plans in the critical illness (CI) category have been introduced, such as the Bajaj Allianz Health Insurance Women’s Health Insurance-CI Plan and the HDFC ERGO General Insurance Women CI Comprehensive Plan, which are designed for women, including homemakers.

Max Life Insurance recently launched a specific term insurance plan for women homemakers—Max Life Smart Secure Plan. The policy takes into account financial documents in the homemaker’s name, including bank statements, ownership of a car, investment portfolio, etc. “Max Life has taken the initiative to offer standalone protection plans to homemakers regardless of their spouse’s insurance. We have seen robust numbers in this segment,” says Aalok Bhan, director and chief marketing officer, Max Life Insurance.

Then there are credit cards specifically meant for women such as HDFC Solitaire, Standard Chartered Landmark Rewards Platinum, Kotak Silk Inspire and Citibank Rewards. Homemakers, too, can apply for such cards if they have a bank account and fixed deposits in the respective banks.

***

Control Your Financial Reins From Home

Deepika Asthana

Life events such as marriage or birth of a child or taking care of elderly family members often lead to women taking a break from their career. This does not, however, necessarily need to impact your financial security or come in the way of achieving financial independence. Here are a few ways to continue earning an income.

Become a mutual fund distributor: If you have an interest in financial planning and believe that with the right financial advice individuals can create robust portfolios, you can consider becoming a mutual fund distributor. As a distributor, you earn a fee for every mutual fund investment that your clients make and continue to earn as long as your client remains invested. It is fairly simple to become a mutual fund distributor. Register for the National Institute of Securities Market (NISM) VA Mutual Funds Distributors Certification Exam, pay a fee of Rs 1,500, clear the test and get certified. Go through the Know Your Distributor process, and get a Association of Mutual Funds in India (Amfi) Registration Number (ARN). After that, you are all set to register with asset management companies (AMCs) or bigger distributors and start your business.

Start a business on Instagram: In just over 10 years, Instagram has metamorphosed from a simple photo sharing app to a thriving business ecosystem. According to 2021 data from a paper published on Hootsuite, more than 1 billion people use Instagram every month, and roughly 90 per cent of them follow at least one business. This means that if you are, say, a content creator, home baker/chef or can do small-scale manufacturing, you don’t need to worry about the cost of attracting clients. You can leverage your skills and set up shop by simply using Instagram for business.

Become a freelancer: As an individual, you might have several skills that can add value to people and the society at large. There was a time when being a freelancer was not easy as there were very few ways to reach out to people. However, today, due to the rise of the gig economy and the demand for customised solutions, freelancers can explore a much larger ground. Edtech and digital content sites can be good starting points. You might not necessarily achieve instant success, but it would put you on the path to productivity and potentially generate income.

Today, there are many flexible and part-time opportunities. So, celebrate the twists and turns of life and have faith in your ability to stay financially secure. The world is still your oyster.

The author is a financial market expert

The writer is a freelance financial journalist letters@outlookmoney.com