Bengaluru resident Sanchita Guha (26) works in an IT firm and draws a fairly good package. However, at the end of every month end she is always running out of cash.

In a routine fashion, the credited salary gets exhausted almost by the mid of the month after paying all the bills, EMIs, insurance premium and credit card payments. The next month, the same viscious cycle continues.

Guha’s case is a classic example of paycheck to paycheck living. It is an ailment that not only plagues youngsters who have just started working and are not seriously thinking of their financial future, but just about anybody. Leading such a life might seem very common and is also the subject of many social media memes, but it comes with some serious risks. In fact, it is much like a quicksand pit escaping from which becomes quite a task.

The risks associated with such a paycheck to paycheck lifestyle are many. “It means that in case of any emergency, there is absolutely no readiness,” stated Shweta Jain, certified planner and Founder, Investography.

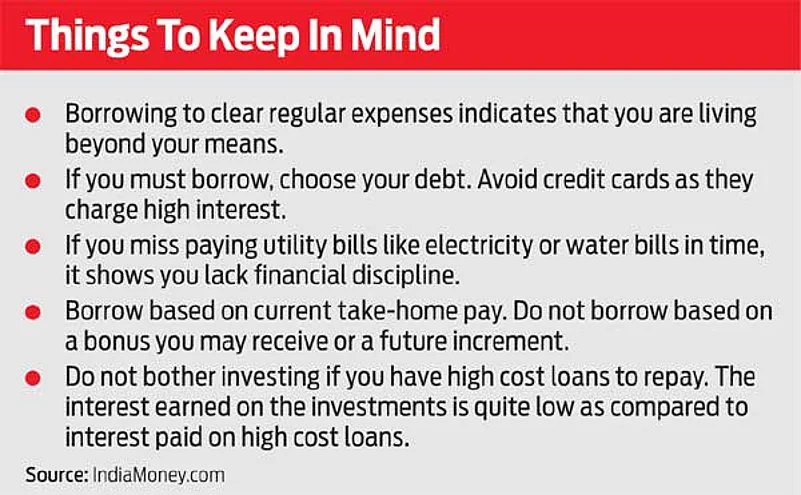

Emergencies do not really arrive with prior notice, and if unprepared, one will need to resort to personal loans in order to survive. Nowadays, availing a personal loan is just a click away with the money being processed to your account within a few working days. This marks the beginning of a series of trouble—falling into a debt trap and credit card usage, making it even worse.

The bill adds up and when the time comes, one does not have enough money to pay the dues.

People often resort to paying the minimum balance on a credit card in order to continue with its usage. “It soon becomes a habit and credit card outstanding keeps increasing. Credit cards charge 24-36 per cent a year on outstanding dues and you land into a debt trap,” said CS Sudheer, CEO and Founder, IndiaMoney.com.

This has other financial implications—outstanding debts and non-repayment of debt, which eventually impacts a person’s credit score. “Additionally, you will have to compromise on living standards and are likely to fall prey to stress which affects your work life, health and even relationships,” Sudheer further added.

The question naturally arises as to why so many people end up in such a situation? We are often told that our parents, whose incomes were modest, never lived a paycheck to paycheck life. This is often considered as something that one can associate with the youth of the time. Understanding the reasons is key to bring in financial discipline which helps one to get out of it.

“Easy availability of credit through multiple sources is one of the primary reasons that many youngsters fall into this trap,” said Uday Dhoot, Partner, Venn Wealth. A new high-end smartphone might cost approximately Rs75,000 and one would mostly not have enough cash to purchase it; but a credit card EMI over 12 months makes the sum look manageable.

The temptation to buy a phone is thus higher because such a loan does not even require any documentation and one only needs to choose the credit card EMI option during checkout. EMI worth Rs6,000 every month may not seem a big deal, but several such purchases only tend to add up to the monthly credit card bill. People, especially youngsters, spend more on wants than on needs, majorly due to pressure from their peers.

“Treating credit cards and payday loans as emergency fund is a bad idea. Youth spend the entire paycheck and then use loans to fund unnecessary spends. This leads to a debt trap,” said Sudheer.

All these stem from a simple fact of ignoring financial planning basics. “By not setting a financial goal, there is no incentive to save, invest and borrow money wisely; the consequence is living from paycheck to paycheck,” he added.

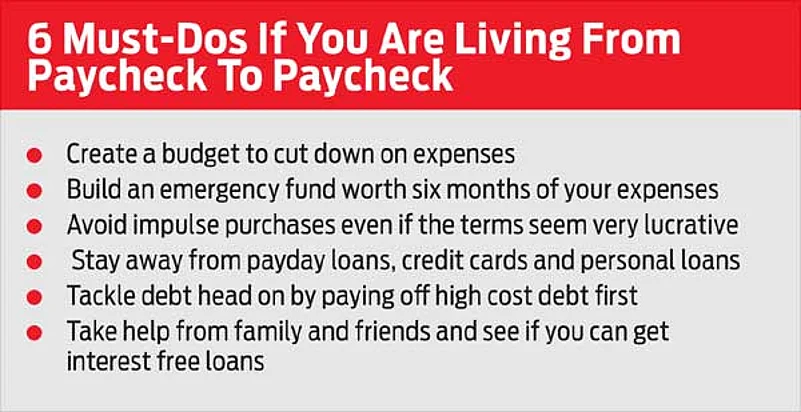

If you can identify with paycheck to paycheck living, there is both good and bad news. The bad news first. Your situation will not improve without taking any action, nor will it improve with just wishing it away. Now, the good news. Some basic financial measures coupled with self-discipline is all that is required to get out of such a situation. Here is a list of things to follow if your salary seems to vanish from your account much before the end of the month.

The first and most important thing to do is budgeting. A budget is nothing but keeping an account of every penny that is spent and earned. “A budget makes sure you have money for things which are important by prioritising your spending,” said Sudheer.

The idea is not just to cut down on expenses but see where your hard-earned money is going so that necessary adjustments can be made. Only when one has a budget can one have a surplus, thereby managing to come out of debt and eventually start with one’s savings.

Following a strict budget on a regular basis will help ensure that you are able to cut down on uncessesary expenses and live well within your means.

“Cutting down on subscriptions of things you do not use, eating at home more or restricting the number of eating outs, trying to use public transport and not depending on Ola or Uber are some of the ways one can do that,” explained Dhoot.

Avoiding debt is crucial because if one has a lot of EMIs to pay every month, the salary is not likely to last for long. Earlier generations waited to accumulate money for a serious purchase, be it a home or a car. “We have an option to avail loans even for our marriages and vacations. It is easy to get into these, and very difficult to get out, once stuck in,” said Jain. “The tendency to stretch beyond one’s means is easy, it is a slippery slope. If you cannot pay fully for something, don’t go for it,” she further added.

Sudheer suggested, it is wise to follow the 30 day rule in order to avoid impulsive purchases. According to this rule, even after a month if you really think that you need the product, go for it. Also when going for a loan or credit card EMI to purchase a product, take a close look at interest rates and your ability to repay.

Getting out of existing debt is also crucial as it is the main culprit. The best way is to avoid falling into a debt trap, but once in it, one needs to find a way out. This needs to be taken seriously as it is the root of all problems. Paying off high cost debts on priority is the first thing to do. “Personal loans charge as high as 15-17 per cent a year and credit card debt around 24-36 per cent a year. You can avail secured loans against your fixed deposit to pay off high cost debt as interest rates are low,” said Sudheer.

He further added that one can take help from family, ask for interest-free loans and clear off any debt with that. In the worst situation, Dhoot suggested that one should speak to a debt specialist to find out some sort of settlement with the loan company.

Since not being ready for any financial emergency is one of the biggest pitfalls of living from paycheck to paycheck, creating an emergency fund is crucial. It is the most basic personal finance mantra, which people tend to neglect.

Having six months of expenses in your savings account or in liquid funds is mandatory, and this money should be touched, as the name makes it clear, only in emergency. It is time to make your salary count!

anagh.pal@outlookindia.com