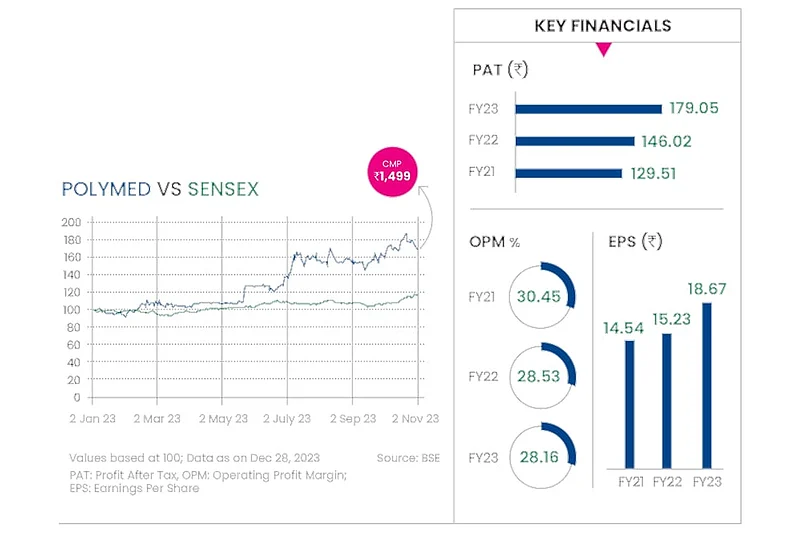

Company Name Poly Medicure

Current Market Price Rs 1,499

Calendar Year Return 65.53%

***

Poly Medicure is a leading name in the healthcare sector in India and our core pick in this space.

Investing Rationale

Growth: The company is well-positioned to register growth in domestic business due to several factors. These include growth in infusion therapy and/or renal care segments, demand growth in export business, which is to be mainly led by the Europe market and is expected to fetch the company market share as well as new customers, launch of (class II) infusion products in the US, which is expected to generate revenue of $15-20 million annually in the next four years, and lastly, higher export revenues.

Exports: Export revenues contributed to 64 per cent of total revenues and showed strong growth of 25 per cent year-on-year (y-o-y) and 7 per cent quarter-on-quarter (q-o-q) led by nfusion therapy segment (which contributed 85-88 per cent of exports).

New Products: The company has also filed for few infusion-based therapy products in the US and awaits 510,000 approvals at the end of FY23, which has the potential to generate sales of $15 million over the next five years. We expect an export revenue of 18 per cent CAGR over FY22-25 with increase in penetration in Europe, the US and Asia.

Domestic Market: It has 2.5 per cent market share in Indian medical consumables, with a market size of Rs 141 billion. It is likely to benefit from untapped potential led by change in regulatory landscape with a shift towards organised players.

A strong balance sheet and cumulative free cash flow generation of Rs 4.7 billion over FY24-FY26 bodes well.

Revenue: We expect an overall revenue of 24 per cent CAGR over FY23-26 led by new launches of vascular products in cardiac and critical care segment and ramping up the renal segment in domestic business, along with export revenue of 24 per cent CAGR with increase in penetration in Europe, the US and Asia. We believe that the management has set a good base for the growth to take off in the medium term. Local regulatory risks apart, we believe volatility in currency movement can be a risk to core earnings.

We recommend buy at a target price of Rs 1,822 at 42x FY26 price-to-earnings (P-E), at 20 per cent premium to its eight-year historical mean.

The company trades at a premium in its valuation, and this can be justified by two key factors. First, there is no direct listed peer, especially considering that global counterparts primarily operate in the high-tech medical equipment sector with a substantial presence in mature markets, which provides a foreseeable opportunity for Polymed. Second, Polymed exhibits a faster growth trajectory in both sales and earnings compared to its peers.