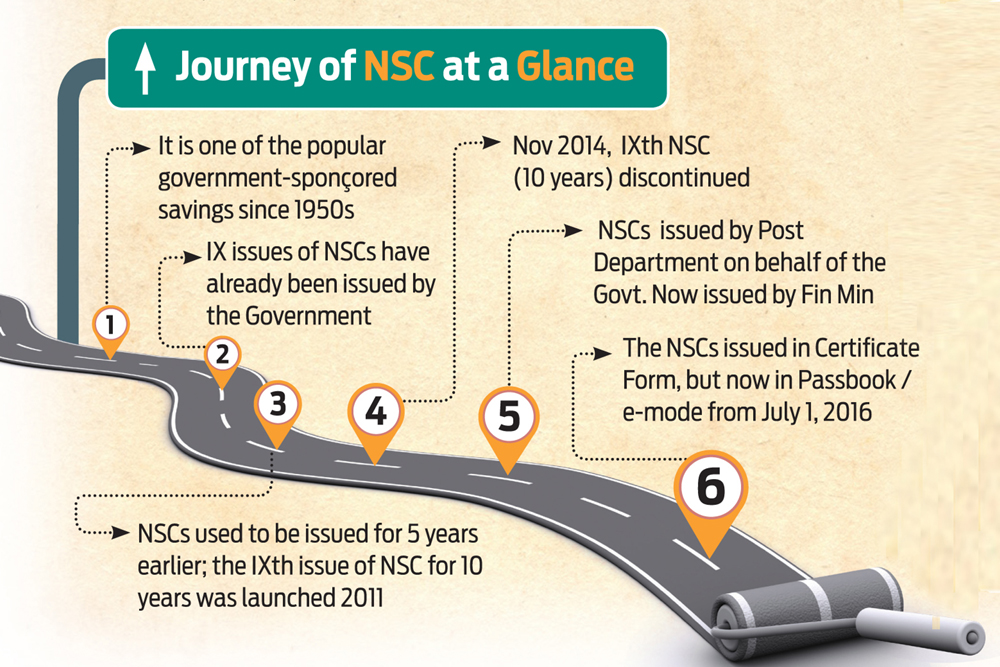

Sushweta Ghosh, a senior writer with a leading publication in India is a regular investor in National Savings Certificates (NSC). It formed a major part of her investment in the 1990s, but the last time she purchased a certificate was in 2007.

“It was a much sought-after investment, but my nieces and nephews don’t even know such a scheme exists; they are all into Mutual Funds big time,” says Ghosh. She has redeemed all her NSC certificates fully now, since there are more attractive options in liquid mutual funds.

There are many like Ghosh in India, who have lost interest in NSC and youngsters have almost forgotten about it. “NSC was integral to my investments, tax saving was secondary…no, my son who is in government service does not even know such a scheme exists,” says VV Ramachandran, a retired auditor.

To renew the interest and to make it an attractive investment option, the Finance Minister Arun Jaitley in the Union Budget 2018–19 had proposed to subsume NSC, under a new Act. NSC is now covered under the Government Savings Banks Act, 1873.

With a common Act, implementation is easier for depositors as they need not go through different rules and Acts for understanding the provision of various small saving schemes like NSC.

Apart from ensuring existing benefits, certain new benefits to the depositors have also been introduced.

Like Investment in NSC can be made by the guardian on behalf of minor(s). The guardian may also be given associated rights and responsibilities.

There was no clear provision earlier regarding deposit by minors in the existing Acts. The provision has now been made to promote the habit of savings among children.

The new act provides for operation of accounts in the name of physically unfit and differently-abled persons, which was absent in the previous Acts.

Rights of nominees have now been more clearly defined. Earlier provisions of the Acts stated if depositor dies and nomination exists, the outstanding balances will be paid to nominee(s). Whereas, Supreme Court in its judgment stated that nominee(s) is merely empowered to collect the amounts as Trustee for the benefit of legal heirs. It was creating disputes between the provisions of the Acts and verdict of Supreme Court.

The earlier Acts were silent about grievance redressal. The amended Act allows the Government to put in place mechanism for redressal of grievances and for amicable and expeditious settlement of disputes relating to Small Savings.

Further no change in interest rate or tax policy on small savings scheme is being made through this amendment.

“The biggest attraction was IT exemption under section 80C, but the Rs1.5 lakh limit usually gets exhausted with investments in insurance and Public Provident Fund (PPF) which is one of the reason for NSC being almost forgotten by even traditional investors,” says Tarun Birani founder and CEO TBNG Capital Advisors Pvt Ltd.

rajendran@outlookindia.com