It is a generally accepted notion that unit-linked insurance plans (Ulips) are not investor-friendly due to their relatively higher charges and lack of flexibility in exiting from a policy, apart from shifting from one sub-fund to another. It is usually recommended that investments should be executed through mutual funds (MFs), and for matters of insurance coverage, you should buy term insurance.

This view is correct. However, today we will look at certain other aspects of Ulips. If you are approached to buy a Ulip, or if you are considering one and want to compare it with mutual funds, then here are the things you should be looking at.

Factors For Comparison

The most important element for comparison, is the charges on the product. You may say performance is most important as that is what you get as returns, net of charges. However, future performance is by definition, unknown. You can look at historical performance for only getting a perspective.

If a Ulip fund is underperforming, you can shift from one fund to another like from equity to debt, but it is difficult to exit from the product. Charges are the biggest contention between Ulips and mutual funds, and it is something measurable.

Quantifying Charges In Ulips

Long ago, Ulips came with very high front-loaded charges, which was deducted from the premium that you paid, and was passed on to the intermediary. Even now, there are front-loaded charges that are on the higher side.

From the earlier days of excessive front-loaded charges to current times of relatively-lower-but-still-on-the-higher-side charges, there was a regulation passed by the Insurance Regulatory and Development Authority of India (Irdai) in 2010. Rather than putting a cap on front-loading per se, the cap was put on overall charges. This was referred to as “reduction in yield”.

Concept Of Reduction In Yield

The Irdai circular dated June 28, 2010, said that “the net reduction in yield for policies with terms less than or equal to 10 years shall not be more than 3 per cent at maturity”.

It laid down the maximum permissible reduction in yield, as per the tenure of the policy, such as 5 years, 10 years, etc.

The reduction in yield refers to the difference between the total and the post-cost return. This was an indirect way of capping costs in Ulips.

Charges in Ulips

There are typically four categories of charges in Ulips.

- There is a front-loaded charge, also known as premium allocation charge, which is a euphemism to camouflage it from intermediary remuneration.

- Then there is a fund management charge—what you pay the insurer to manage the investment component of the fund. It is reflected in the net asset value (NAV) which means the NAV is declared post the fund management charges. It is capped at 1.35 per cent of the fund value. This is similar to mutual funds as mutual funds also have fund management charges, sometimes higher than 1.35 per cent, but the similarity ends there. Mutual funds have fund management charges, known as total expense ratio (TER) which includes all charges and/or expenses. There are no other charges in mutual funds.

- Policy administration charges are usually deducted by cancelling units of your Ulip.

- Mortality cost, the true cost of insurance, is deducted by cancelling the units.

Insurers can charge you extra, apart from the four categories of charges mentioned above, if the policy offers a guaranteed return.

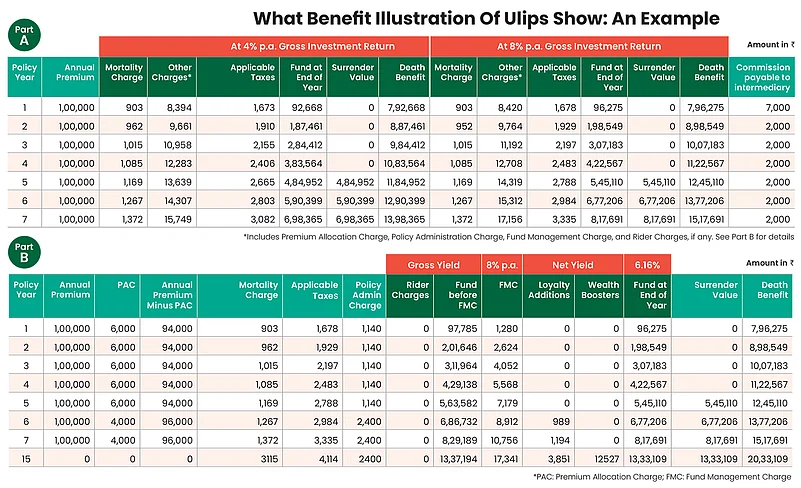

According to Irdai regulations, the charges should be levied to an extent that the reduction in yield mentioned earlier, which is the difference between gross yield and net yield, is not more than the limits mentioned. These costs are shown to you through a ‘benefit illustration’ (see table on the right), assuming fund growth rate of 4 per cent and 8 per cent. Do note that the reduction in yield does not take into account mortality cost, which is the true cost of insurance.

Benefit Illustration

Insurance providers have software where the sales executive and/or agent in touch with the customer would put in the relevant details like name, age, amount of premium, term of the policy, etc. The system will throw out the benefit illustration with assumed returns of 4 per cent and 8 per cent per year.

In this illustration, the insured person pays a premium of Rs 1 lakh per year, for seven years. The front-loaded premium allocation charges are Rs 6,000 for the first five years and Rs 4,000 for last two years. Net of the front-loaded charges, the remaining amount of your premium of Rs 1 lakh gets invested.

At the end of the first year, net of all the charges mentioned earlier, your amount grows to Rs 92,668 at a growth rate of 4 per cent, and to Rs 96,275 at a growth rate of 8 per cent. The fact that the amount is less than your first-year premium of Rs 1 lakh means only the net amount, net of front-loaded charges, got invested.

At the assumed growth rate of 8 per cent, your fund amount is Rs 13,33,109, at the end of the 15th year. The net yield to you, as worked out by the insurance company, is 6.16 per cent. That is, the reduction in yield is 1.84 per cent. To reiterate, mortality cost is not part of reduction in yield—1.84 per cent—is calculated without taking mortality cost into account.

On the face of it, this figure of 1.84 per cent does not look like a very high charge, as some mutual funds have similar expenses charged to the scheme. However, in the initial five years, premium allocation charges are 6 per cent per year. Given that it is a 15-year policy and from year 8 to15, there are no premium payments and front-loaded charges, it has been made up by returns from the market at the assumed rate of 8 per cent, and the compounding effect on returns.

Conclusion

For comparison with mutual funds, look at the benefit illustration of a Ulip. To reiterate, in a Ulip, exiting from the policy is difficult. Contrary to this, mutual funds offer you greater flexibility in that regard.

By Joydeep Sen, Corporate Trainer and Author