Justice Oliver Wendell Holmes of the US Supreme Court made a famous remark on taxes a few years ago. “Taxes are what we pay for a civilised society. I like to pay taxes because with them, I buy civilisation”. In the context of India, can tax-paying citizens really expect to buy civilisation? Perhaps not.

Every year, the Government of India collects crores of rupees in taxes from its citizens. Yet for decades, it has not been able to provide basic amenities such as potable water, security, and tolerably good education and healthcare to its people. Instead the opposite is true.

The country’s citizens have been paying for these services on their own and at the same paying income tax to the government. In such a scenario, one can legitimately pose a question: why should anyone want to pay income tax?

There is general reluctance among people to pay income tax for several reasons. For one, the government has not been able to provide basic amenities. The second disinclination to pay taxes is the indiscreet use of taxpayers’ money by a government that lacks accountability. Thus, the desire to evade taxes, especially income tax, is natural. Thirdly, tax benefits are realised by resorting to tax evasion, avoidance and tax planning.

Tax avoidance denotes tax minimisation

Evasion implies concealment and furnishing of inaccurate particulars of income. Considered a social crime, it is punishable by penalty or prosecution. On the other hand, tax avoidance denotes resorting to tax minimisation by taking benefit of exemptions, deductions and incentives provided under Income Tax Act, 1961. It can be of two kinds: illegal and legal. Illegal tax avoidance implies circumventing provisions of the Act to gain unintended tax cuts. Legal tax avoidance – which means ‘tax planning’ in refined words - implies taking advantage of all exemptions, deductions, incentives and benefits provided within the framework of the income tax law.

Tax avoidance is not only legal, but also ethical. Jagdishan J, in the 1965 case of Aruna Group of Estates versus State of Madras had said: “Avoidance of tax is not tax evasion and it carries no ignominy with it, it is sound in law and certainly not bad immoral for anybody to so arrange his affairs as to reduce the brunt of taxation to a minimum.” In 1973, the Supreme Court in the CIT versus Calcutta Discount Co. Ltd. case observed that “It is a well-accepted principle of law that an assessee can so manage his affairs as to minimise his tax burden”.

‘Avoidance of tax liability is not prohibited’

In the UK, the concept of tax avoidance came in for discussion in a big way following a 1936 IRC versus Duke of Westminster case. In the matter, Lord Tomlin thus observed: “Every man is entitled, if he can, to order his affairs so that the tax attaching under the appropriate Act is less than it otherwise would be. If he succeeds in ordering them so as to secure this result, then, howsoever, unappreciative the Commissioners of Inland Revenue or his fellow taxpayers may be of his ingenuity, he cannot be compelled to pay an increased tax”.

A similar view was expressed by Justice J C Shah of the Supreme Court in the CIT versus Raman & Co case in 1968, where the learned Judge, inter-alia, observed: “Avoidance of tax liability by so arranging commercial affairs that charge of tax is distributed is not prohibited. A taxpayer may resort to a device to divert the income before it accrues to him. Effectiveness of the device depends not upon consideration of morality, but on the operation of the Income Tax Act. Legislative injunction in taxing statutes may not, except on peril of penalty, be violated, but it may lawfully be circumvented”.

The debate on tax planning was initiated in the country by Justice O Chinnappa Reddy, who emphatically denounced tax planning. However, the majority view in this case was expressed by Justice Ranganath Misra, who concluded by saying: “Tax planning may be legitimate provided it is within the framework of law. Colourable devices cannot be part of tax planning and it is wrong to encourage or entertain the belief that it is honourable to avoid the payment of tax by resorting to dubious methods. It is the obligation of every citizen to pay taxes honestly without resorting to subterfuges”.

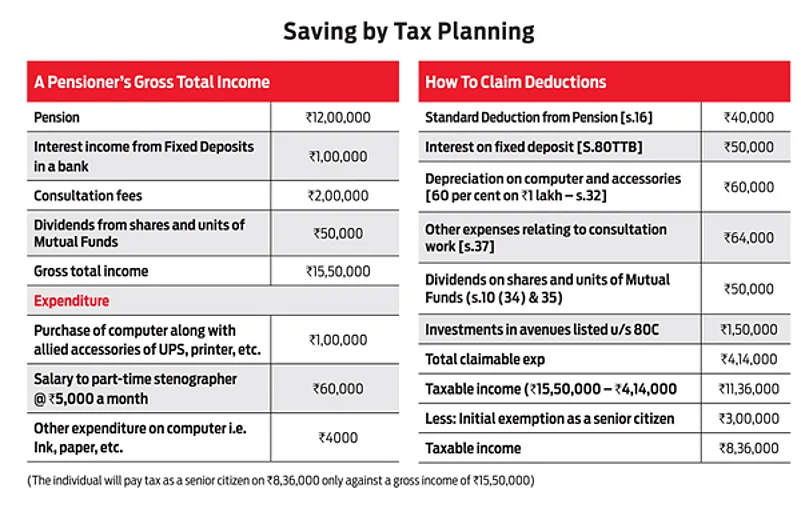

Taxes can be saved by taking advantage of exemptions

Thus, discussions on the concept of legal tax avoidance and tax planning have been going on for quite some time and the settled legal position now is that tax can be saved by tax planning (see chart) within the framework of law. It could be attained by taking advantage of permissible exemptions, deductions, incentives and tax benefits provided under the Income Tax Act.

Some of these include:

Standard deduction upto Rs40,000 in a year can be claimed by salaried employees and pensioners.

Hindu undivided families can lessen their tax burden by partition.

Companies can claim numerous tax benefits by compliance to conditions stated in Chapter VI A of the Income Tax Act.

Deduction of Rs50,000 from interest on FDs can be claimed by persons of 60 years or more u/s 80TTB.

Income from dividends and units of mutual funds is exempt from tax.

Deduction upto Rs1,50,000 is permissible for investments in avenues stated in Section 80C of the Income Tax Act.

Depreciation at varied rates on various aspects mentioned in Section 32 of the Act is allowable. Rate of depreciation is 60 per cent for computers and its accessories.

There are number of other benefits provided under this Act. A detailed reading should provide a comprehensive understanding of some of these benefits that you could use.

The author is former Chairman, CBDT