That breath of relief you take, when you pay that last installment of your loan is probably one of the most memorable moments. Needless to say, a sense of accomplishment prevails when you achieve a feat like this. Whether you have availed home loans, where your home is mortgaged, or a car loan where your vehicle is hypothecated, a proper closure of the loan is essential. And when it comes to a loan closure, if a borrower does not adhere to certain processes, it might lead to several problems in the future.

Having said that, every bank has its own checklist when it comes to pre and post closure of loans, which borrowers must adhere to. Usually, a personal loan can be closed in three ways, which include regular closure, foreclosure or preclosure and part-payment. “The right or wrong way to go here is decided by your financial situation and can differ from person to person,” explained Gaurav Chopra, CEO, IndiaLends.

The regular mode of closing a loan, consists of fixing a certain amount as monthly EMI and repaying it on time. In case of pre-closure, a borrower usually repays the loan when she has received a lump sum amount at once, which is equal or close to the outstanding loan amount and closes her loan before the tenure is complete.

When it comes to part-payment, although a person has a large sum of money, it is not equal to or has less than the entire principal outstanding loan amount. “Part-payment involves the borrower paying an amount more than a fixed number (generally more than two) of EMIs depending upon the bank. This leads to lowering of the outstanding principal and thereby the accrued interest. You can opt for this method if you have extra money but not enough to completely repay the loan amount,” said Chopra.

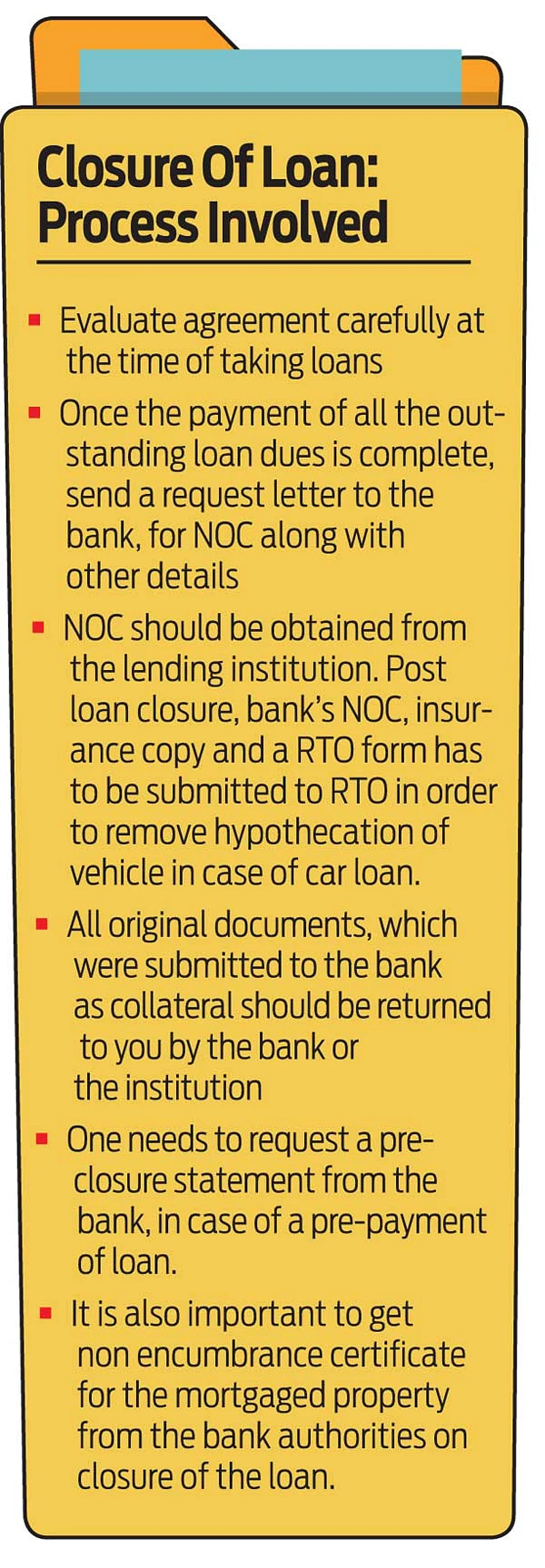

Usually the paperwork for repayment, is done at the time of availing the loan itself. A borrower needs to carefully evaluate the loan agreement and understand it, because, once it is signed, she must legally abide by the terms and conditions. Procuring the closure letter in the form of No Dues Certificate (NDC) or No Objection Certificate (NOC) or closure letter from the bank or financial institution is the first step towards closing a loan.

In case of car loans, the borrower has to approach the regional transport office (RTO) for getting hypothecation removed. Further, in case of car loan or two-wheeler loans closure, prepayment charges are levied especially by traditional institutions. “At the time of prepayment, the total outstanding principal amount is to be repaid along with penalty charges and GST. Post which, NOC should be obtained from the lending institute. One would also like to remove bank’s hypothecation of vehicle. Post loan closure, bank’s NOC, insurance copy and a RTO form has to be submitted to the RTO,” said Vikas Kumar, CTO and Co Founder, LoanTap. In case of a foreclosed loan, a borrower needs to ensure that she cancels any post-dated cheques that might have been issued to the bank earlier.

When it comes to housing loan, once the loan repayment has been completed, one will have to write a letter to the bank, requesting for a NOC stating details like residential address, borrower’s name and loan account number. The letter should also mention that all dues have been cleared by the borrower and the lender does not have any claims in the property. “Collection of all original documents of home that were given to the bank or HFC at the time of taking loan is crucial. The institution must remove lien on the property and update the borrower’s CIBIL score. Finally, a check on destruction of post-dated cheques submitted to the bank or HFC at the time of taking the loan is must,” explained Kumar. Post all the processes with the bank, the owner must apply for a fresh non encumbrance certificate from the registrar office.

That said, when it comes to any property, which was earlier mortgaged with the bank for obtaining the said loan, the NOC shall be produced at the registrar’s office if such mortgage was a registered one for clearing bank’s lien over the said property. However, if the mortgage was unregistered, then the return of title deeds of the said property by the bank authorities shall suffice. “It is advisable that when the loan facility is obtained from the bank, the account holder obtains the List of Documents (LoD), from the bank’s custody. Since the tenure for property loans is long, the LoD obtained would be handy to reconcile and ensure that all relevant documents have been returned by the bankers at the time of closure of the loan,” said Suresh Surana, Founder, RSM Astute Consulting Dealing with aftermath of loan closure is also something that one needs to consider. Proper closure of a loan is very essential in order to ensure that the bank clears the borrower of the debt claims from the said loan. The borrower can inform CIBIL(credit information company) about his or her loan closure, via the bank or lender, which normally takes 30 days. Commenting on the significance of closure aftermath, Surana said,“In case, all the property documents are not returned by the bank after closure of the loan, the borrower might find it difficult to sell off the property in future or obtain another loan by mortgaging the said property. Similarly, it is important to obtain no encumbrance certificate for the mortgaged property from the bank authorities on closure of the loan.”

As simple as it seems, but if your loan is closed incorrectly, then it might affect your CIBIL score and consequently influence your creditworthiness, which in turn can have a negative impact on your future borrowing of loans from other banks or financial institutions. Closing your personal loan is an important duty, which should not be neglected at any cost.

Be aware of the procedures involved in properly closing your loan to avoid any problems related to your credit.

himali@outlookindia.com