Medical practice is a profession that is considered a special mission, a devotion. Every day, doctors see patients’ pain and suffering from close quarters. Then, they give them the required treatment to provide comfort. When it comes to the financial lives of doctors, things are very different. They are just like any other common investor. Dr. Charan Kamal (49), Head Surgeon of a well known eye hospital in Amritsar, had been investing in traditional products like Post Office schemes but was uncomfortable being not well-versed with their utilities.

Due to his busy schedule and ophthalmologist duties, he had obliged whosoever approached him with investment products. We can well imagine what happens when an investor obliges every financial product seller in that way. There is a long queue, and we are not just talking about patients! Consequently, over the years Dr. Kamal had accumulated a portfolio filled low-return products. Always in a race against time, the doctor in him took precedence over the investor in him.

Then one fine day, he was explained about the importance of managing funds in a professional way. Dr. Kamal immediately fixed an appointment with us. We made him aware of the future value of his forthcoming responsibilities about his children, Gurkamal (19) and Jaideep (13) and also charted a way for his retirement planning.

Jasbir Kaur (Dr. Kamal’s wife) a practicing gynaecologist, expressed keen interest and wanted to contribute towards it. Both the doctors mentioned that their combined annual income ranges from Rs25-30 lakh. This income provided a good stepping stone to gain financial independence and chase financial goals. So, we categorizsed their financial plan into the following:

Asset allocation is the key to any successful plan. Studies show that proper asset allocation is the single biggest factor driving portfolio returns. After understanding his requirements, Dr. Kamal was suggested an asset allocation of 50-50 towards debt and equity. The 50 per cent debt was for liquidity needs which will arise within five years. The 50 per cent allocation towards equity was for their own retirement planning, seed capital for kids establishments and other future events. This 50-50 approach provided safety and growth in equal measures.

On observing that the couple were thoroughly under-insured, we proposed an insurance cover of Rs2 crore each in order to take care of their long-term aspirations up till the age of 85 (insurance cover needs to be revisited every three to five years). Also, we proposed a professional indemnity cover of Rs1 crore each considering the risky nature of their profession.

Lastly, we recommended them to insure their house and hospital premises for fire, burglary and machinery breakdown. Just like human lives, immovable assets should be adequately covered against financial harm due to unforeseen events. This adds an extra layer of protection.

As ironical as it may sound, the doctor couple was observed to be insufficiently covered for medical contingencies. Despite being aware of rising medical costs, somehow in their busy everyday lives, the need to financially protect themselves from healthcare costs had been missed. So, we recommended an additional floater cover of Rs50 lakh(with Rs50 lakh recharge benefits) for medical contingencies. Proper medical cover will shield their savings and investments from any sudden healthcare cost event.

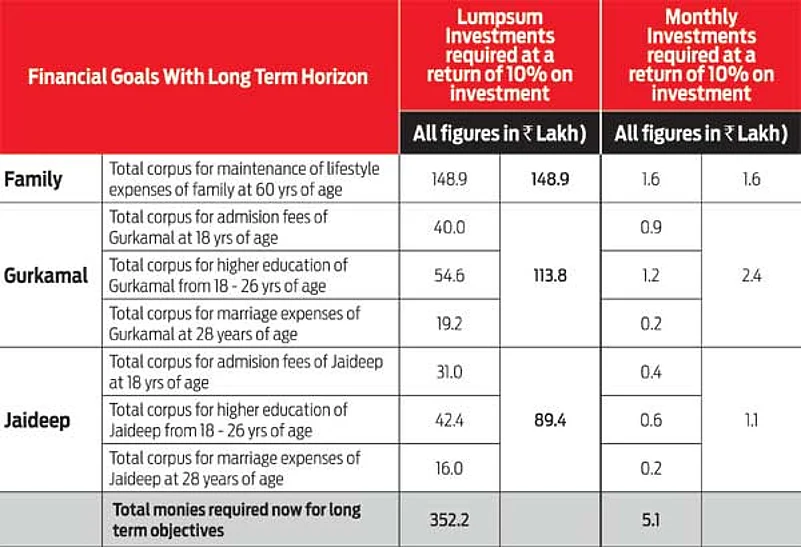

Ambitions help us grow and test our limits. Guidelines have been provided to Dr. Kamal for the education and marriage of his children, his golden years’ planning and their dream project of a new hospital. These guidelines are calculated in accordance with the real rate of returns (inflation-adjusted return).

We divided the portfolio recommendations into two parts:

- Short-term portfolio to take care of their requirements over the next four-five years and likely to be invested in various debt funds.

- Long-term (LT) portfolio to take care of their requirements from the fifth year onwards Portfolio LT to be invested in diversified equity funds (five years and above).

Dr. Kamal currently is investing Rs85,000 per month. A contingency corpus has also been invested in an array of debt funds, ranging from liquid to mid-term plans. Also, Kamal is holding about 58 per cent of his assets in debt and strategically moving towards reducing it to 50 per cent over the period of time.

We also advised Dr. Kamal to set up a Hindu Undivided Family (HUF) plan, to reduce the tax burden. We take quarterly updates from him too. During activation of his financial plan, he was advised for setting up of an ultra-modern hospital (his dream), for managing funds from his own source and from the bank. He successfully completed the project, acknowledging my contribution. Dr. Kamal teaches us that executing a financial plan to the minutest detail is as important as planning for it.