For Amudha, life was an irony between her identity and the reality she lived in. Her Tamil name referred to the wealth of Ambrosia, but all she had was a handful of dreams fostered deep in her mind. She didn’t know how she could give her three daughters a life better than what destiny had unleashed for her. Krishna, her husband and a farmer, could ensure a reasonable living for his family but his income was not enough to make Amudha’s dreams come true. He could save no more than Rs 1,000 or so a month during the harvest and would spend up all the savings during the lean period. The homemaker, in her late-30s, from Sirukadambur village in remote Tamil Nadu, knew that gold was the safest haven for anybody to cradle dreams till they bloom. Alas! With her meagre resource, she could never afford the yellow metal.

The appreciating value of gold makes it the most preferred investment option for the middle and low-income section of the Indian society to fight any exigency and weave their dreams for real.

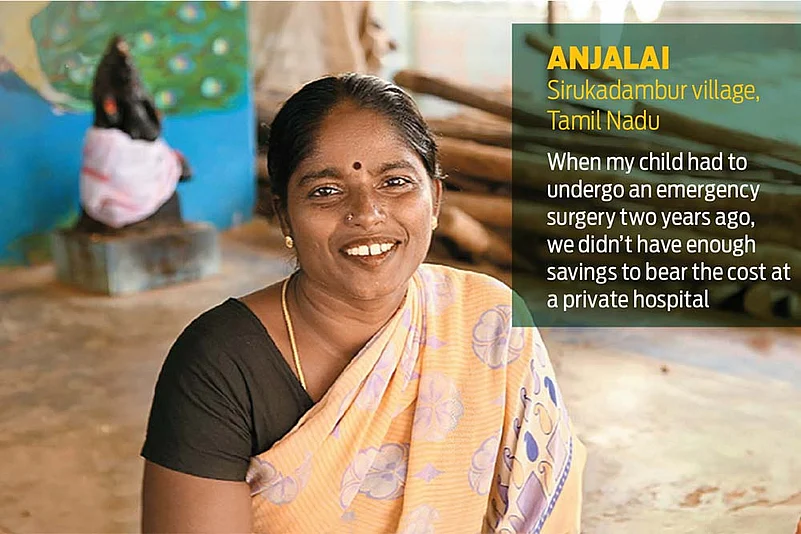

“When my child had to undergo an emergency surgery two years ago, we didn’t have enough savings to bear the cost at a private hospital. We had to take loans from the village moneylender at a steep interest rate and we’re still paying it off,” recalls Anjalai, another villager from Sirukadambur.

A credit-line is often the lifeline for 60 per cent Indians eking out a living from the primary sector or working as daily wage earners. With the government stressing on financial inclusion to bring this huge chunk of unbanked population into the banking ambit, Micro-Finance Institutions (MFI) began homing in aggressively on rural India. The MFIs introduced the flavour of banking to people who were shunned by bigger lenders for their inadequate credentials and low income. It created a room for lenders to tailor their micro-savings products in line with the government’s aim for financialising gold as a productive asset class.

The remoteness of the target customer and the need for an immediate disbursal of loan drove micro-lenders and fintech companies to team up. They devised products and services for a quicker access to credit. The evolving dynamics threw up prospects for products designed to generate income opportunities and preserve a part of the increased earning as rain check. Thus gold became a significant investment instrument.

“If we had gold, we could use it to fund our tractor, instead of keeping the land mortgaged for three years,” complains Amudha. The creditor, she says, lent the money five years ago against a bond to sell their entire harvest to him, for the entire loan period, and at a price he would set.

A Systemic Investment Plan (SIP) for gold seemed to be the best option when Sanjeev Agarwal floated Dvara SmartGold in July 2019. It launched Gold SIP three months later with the objective of creating a financial safety net through gold micro-savings schemes for the vulnerable households, who had been borrowing small loans to meet their immediate requirements.

Gold SIP allows a customer to redeem gold locker balance with gold coins, pendants, cash, bank credit, or get ornaments from a registered jeweller. The company has created a comprehensive digital platform for all services. “I always knew the value of gold, but I didn’t know of a proper channel to save up for it. I was happy to know that by contributing a minimal amount monthly, that gets collected at my doorstep, I will receive a certain assured corresponding quantity of gold after a fixed period,” says Govindammal, who runs a dairy firm on the outskirts of Udayarpalayam in Tamil Nadu.

Dvara Sampoorna Sampath Plan (DSSP) offered by Dvara Kshetriya Gramin Financial Services (KGFS) and Dvara SmartGold includes two schemes – Dvara Dhana Shakti and Dvara Raj Nidhi – customised according to the affordability of the subscriber. It aims to develop a suite of credit, savings, insuranceand investment products as a comprehensive financial plan.

The products lined up under DSSP are personal accident cover, hospital insurance, group term life insurance and Gold SIP. The personal accident cover protects an individual from financial shock caused by loss of human capital as a result of an accident, while Hospi Cash Insurance covers wage loss due to hospitalisation of the customer. The Group Term Life Insurance provides a cover of Rs 2 lakh against untimely death, which can be extended up to Rs 3.5 lakh.

The Dvara Dhana Shakti Scheme has two products – Gold SIP and Hospi Cash. A subscriber can start off with a monthly investment of Rs 500 only and can raise it to Rs 1,500 for a tenure of 24 months.

Dvara Raj Nidhi offers a broader scheme, with Gold SIP, Group Term Insurance, Hospi Cash and Personal Accident Insurance. This has a tenure of 24 months, where one can choose to invest Rs 2,000 to Rs 5,000 every month.

The year-old schemes averaged a 40 per cent monthly growth to reach a corpus of Rs 6–7 crore by the end of the third quarter of financial year 2020-21, despite the pandemic.

“The most encouraging and motivating part of the short journey of the trust has been the fact that even through the most challenging period between April and September 2020, our customers continued to save in our micro-savings regularly,” recalls Sanjeev Agarwal, Founder-Director, Dvara SmartGold. “But that was not all. Thousands of customers enrolled themselves in this period despite a loss in their earnings because of the lockdown.” Dvara SmartGold beat over 400 contestants from over 100 countries in a race to win the ‘Inclusive Fintech 50 Award’ for 2020 in the ‘Savings and Personal Finance Management’ category. The competition showcased early stage fintechs driving financial inclusion.

Dvara has spread out to several class III and IV towns and rural areas of Tamil Nadu, Karnataka, Uttarakhand and Chhattisgarh. The trust is aiming for rural Maharashtra, Bihar, Punjab and Uttar Pradesh in the next few months. “We’re looking at tie-ups with seven categories of partners like MFIs, Business Correspondents (BCs), fintechs, payment aggregators and last-mile delivery platforms,” says Agarwal.

Dvara was incorporated as the Institute for Financial Management and Research (IFMR) Trust in 2007 with an initial seed funding of Rs 150 crore from ICICI Bank. Apparently, Nachiket Mor, former Executive Director of ICICI Bank, was also the chairperson of the governing council of IFMR Trust.

“The structure of the trust is very much like Tata Trust, where all businesses are held under the trust and there is no single financial benefit to any individual. Surpluses are ploughed back into new institutions or into research related to financial inclusion,” Agarwal says.

It has been motivating farmers, farm labourers and daily wage earners to develop the habit of saving.

“Saving should be like bricks, steady and solid, and not like water, always running out. From early days, my mother instilled in me that gold was the best savings, which I can fall back on in case of any financial difficulty. I am relieved that my savings are going to remain with me,” says Anjalai.

yagnesh@outlookindia.com