1 January 2026

Get the latest issue of Outlook Money

When it comes to investing for retirement, mutual funds can be the ideal vehicle to help you secure your future. It has the desirable attributes required to help investors grow their money for ample retirement savings.

However, merely building a corpus is not enough. Achieving a sizeable corpus marks a victory halfway attained; the true measure of success lies in its preservation and ensuring a regular cashflow throughout your sunset days. Mutual funds can help achieve that too through the systematic withdrawal plan solution that is popularly known as SWP.

Let’s understand how an SWP works and how it can help you organise your cash flow post retirement.

What Is An SWP?

An SWP is the exact opposite of a systematic investment plan (SIP). While in an SIP you invest a fixed sum at predetermined intervals in a mutual fund scheme of your choice, SWP allows you to withdraw an amount from your mutual fund investment to your bank accounts at pre-determined intervals for e.g., monthly or quarterly.

You can choose the amount, the frequency and the duration of the SWP according to your cash flow needs. It allows you to choose a fixed amount that you want to withdraw periodically.

How Does An SWP Work For Retirees?

You should remember that you will not require your entire retirement kitty at one go. SWPs can help you get regular cash flow from your existing mutual fund investments over regular intervals. In other words, with the help of SWP, you can get a fixed sum of money regularly on a predefined date.

This facility ensures that you get to access your money easily even as the remaining part of the investment continues to grow well.

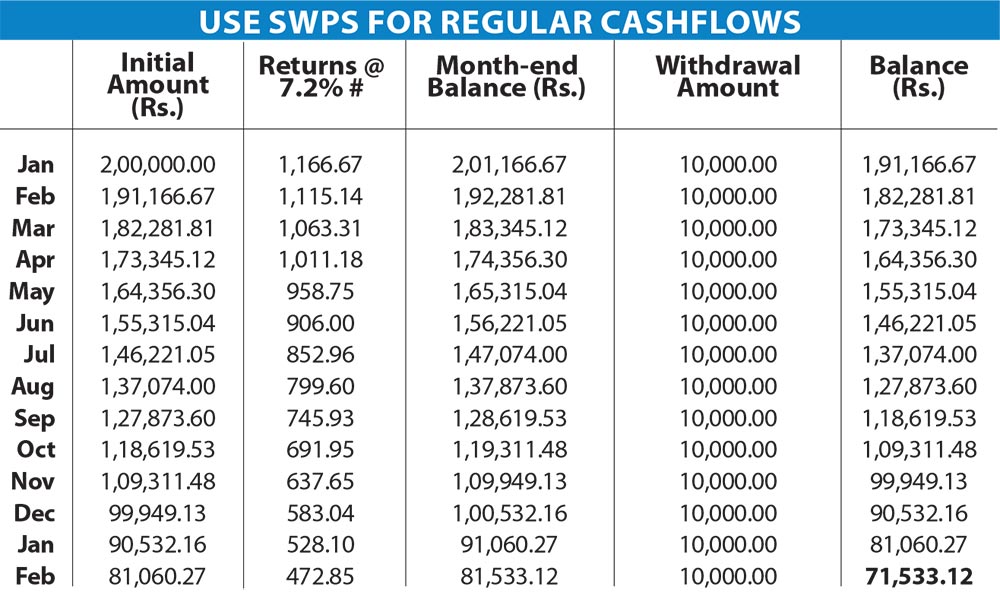

To put things in perspective, here’s an example. Suppose you invest Rs 2,00,000 in a mutual fund and you decide to set up an SWP of Rs 10,000 per month assuming your fund gives a return of 7.2%. In this case at the end of first month, your amount will grow to Rs 2, 01,166.67. You withdraw Rs 10,000 on the first day of the next month, and you will be left with Rs 1, 91,166.67. Again, this amount will grow to Rs 1, 92,281.81 by next month. Similarly, you will again withdraw Rs 10,000 at the end of the month, the corpus will deplete accordingly but is also assumed to grow at the rate of 7.2%.

Things To Keep In Mind

Taxation: Taxation is the critical factor in determining the options. SWPs attract capital gains tax depending on whether your investment is in an equity-oriented scheme or a debt-oriented one.

Exit Load: SWPs are considered as a redemption from the scheme so withdrawals may incur an exit load, depending on the scheme and you can read more about it in the Scheme Information Document.

Conclusion

SWPs can provide regular cash flows and at the same time allow your remaining investments to grow. However, considering the taxation and potential exit load is imperative to make informed decision-making in managing investments effectively.

Disclaimer

Investments made in mutual fund schemes carry market risk and there is no assurance or guarantee that the objective of the schemes will be achieved. The above illustration should not be considered as any guarantee of returns to the investors who are opting for SWP. STCG/LTCG tax is applicable only on the gains made on the redemption units. In case of Systematic Withdrawal Plan (SWP), at the time of redemption of each instalment, investor needs to pay STCG/LTCG tax only on the gains part and not on the invested amount. Thus, it helps the investor over a period of time to consume less principal amount and thereby allowing the balance principal amount to grow further. The calculations are for illustrative purposes and based on the #mean of 10 years rolling returns of the benchmark i.e., 10-year GSec between June 1, 2013 – May 30, 2023: 7.2%. Past Performance may or may not be sustained in the future and is not a guarantee of any future returns. Any calculations made are approximations meant as guidelines only, which need to be confirmed before relying on them. These views alone are not sufficient and should not be used for the development or implementation of an investment strategy. Please consult a financial adviser before making an investment decision.

An Investor Education and Awareness Initiative by SBI Mutual Fund.

Investors should deal only with registered Mutual Funds, details of which can be verified on the SEBI website (https://www.sebi.gov.in) under ‘Intermediaries/Market Infrastructure Institutions’. Please refer to website of mutual funds for process of completing one-time KYC (Know Your Customer) including process for change in address, phone number, bank details etc. Investors may lodge complaints on https://www.scores.gov.in against registered intermediaries if they are unsatisfied with their responses. SCORES facilitates you to lodge your complaint online with SEBI and subsequently view its status.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.