Introduction to Transaction Costs

Buying or selling financial assets such as stocks and bonds carries with it certain costs. In this introduction, we will focus on the bid-offer spread which is one of the costs to consider.

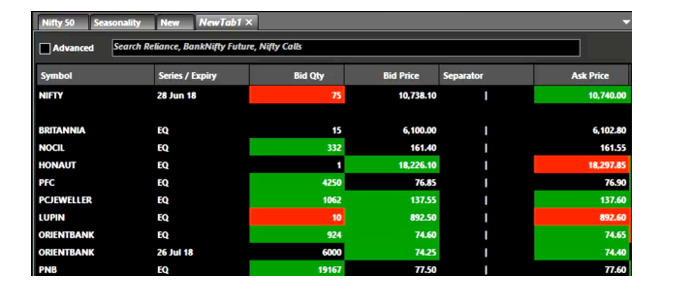

For every traded financial asset, it is typical to be able to find a bid and an offer price in the market. Offer price, or the ask price, is the price at which one can buy the asset while bid price is the price at which one is able to sell the asset. For example, as shown in exhibit 1 below, the bid price of a share of PNB is 77.50 while the same is offered at 77.60. Bid and offer prices exist in the market for the simple reason that buyers are trying to buy at lower prices and sellers are trying to sell at higher prices. Another example of bid and offer prices is the buying and selling rates quoted on foreign currencies by dealers.

Bid-offer spread is calculated as the difference between the bid and offer prices. To illustrate, the bid-offer spread for PNB’s stock is 10 paise in exhibit 1.

Mid-price, which is also a commonly used price measure, is the simple average of the bid and the offer price. In the above example involving PNB’s stock, the mid-price is Rs 77.55.

Exhibit 1: Bid and offer prices of stocks on the NSE

Bid-offer spreads for widely traded stocks such as PNB usually tend to be small given the large number of buyers and sellers. However, at times of market distress, bid-offer spreads tend to increase going up to as high as 3-4 per cent of the price or higher, when a stock is distressed. Recent examples of stocks which have seen wider than normal bid-offer spreads due to stress include Yes Bank, LVB Bank and more recently Vodafone Idea Ltd. Wider bid-offer spreads result in lower returns because, all else being equal, an investor pays a higher price when buying and a lower price when selling. The risk of wider bid-offer spreads (also often described as “deterioration in market liquidity” since it makes it more difficult to buy/sell) has been a concern for investors in recent years. Market liquidity has increasingly been a concern even in well developed markets such as the US treasuries market. Closer home, Franklin Templeton’s decision to close its debt mutual funds in April 2020 which resulted in substantial losses to investors, brought market liquidity in the Indian markets into sharp focus, with some fund managers remarking that liquidity is currently a bigger concern than even the risk of defaults in the Indian bond markets. Market regulators the world over, including Sebi have been aware of market liquidity risk and have attempted to put in place measures to mitigate the risk.

Impact of Transaction Costs on Mutual Funds

Unlike investors who directly invest in stocks or bonds, mutual fund investors invest their money in a fund which pools all the funds to make investments on behalf of all their investors. Mutual fund investments are valued at their Net Asset Value (NAV) which is calculated on the basis of the value of the fund’s investments. NAV of a fund is calculated using mid-prices. When you invest or redeem a mutual fund investment, the mutual fund calculates the value of your investment based on the prevailing NAV of the fund.

To illustrate the problem of transaction costs, let us assume a new investor has invested in a fund. The fund manager decides to invest the money in PNB shares. The fund manager will pay Rs 77.60 per share as shown in exhibit 1.

The NAV, however, is calculated using the mid-price of Rs 77.55. That means that the number of mutual units given to the new investor is based on this NAV; i.e., in other words, the new investor has indirectly invested in PNB at Rs 77.55 while the fund itself has bought the shares at 77.60.

There is a clear loss of 5 paise for the fund in the process. This loss of 5 paise gets recorded as a liability on the day of the transaction and is reflected in the NAV calculation of the following day. In other words, the loss is equally distributed among all the existing shareholders of the fund. Put another way, the transaction costs incurred due to the new investor is mostly borne by the existing investor by way of a lower NAV. A similar loss occurs when an investor redeems as a result of the fund having to sell at the bid price and the NAV being calculated using the mid-price. This is arguably unfair since the existing investors are not driving the transaction costs and ideally should not have to bear them.

In normal circumstances where the difference between the bid and offer prices is small, the impact on the NAV is usually small enough to ignore. However, the difference between bid-offer spreads can become very significant in times of market stress. This is particularly the case in corporate bond markets, which have fewer participants and are less liquid. Therefore, the existing investors of a debt fund could be quite adversely affected due to redemptions or inflows into the fund.

In its proposal to address this problem of existing unit holders having to bear the impact of transaction costs due to inflows or redemptions, Sebi proposes implementing the well-known swing pricing framework. In simple terms, it means new investors or redemptions are no longer calculated using the existing NAV but uses an adjusted NAV which takes into account transaction costs as a result of the investments/redemptions. This will ensure that the transaction costs of new investments or redemptions are borne by the new investors or investors who redeem.

Further, Sebi proposes that it will allow swing pricing to be used at times it deems markets to be stressed.

It is hoped that the swing pricing framework should go a long way in protecting Indian mutual fund investors during times when market liquidity is challenged.

The author is a faculty member, Finance & Financial Technologies, Hero Vired

DISCLAIMER: Views expressed are the author's own, and Outlook Money does not necessarily subscribe to them. Outlook Money shall not be responsible for any damage caused to any person/organisation directly or indirectly.